Land Transaction Tax statistics: April 2019 to March 2020

Our annual Welsh Revenue Authority (WRA) statistical release for Land Transaction Tax (LTT). These statistics provide a greater level of detail, including analysis within Wales.

In this page

Main points

We present these statistics on LTT transactions that we (the WRA) have received by 15 June 2020.

Figure 1.1 below shows:

- estimates of annual data for April 2019 to March 2020

- the percentage change for these headline numbers against previous estimates for April 2018 to March 2019 (made in June 2019)

We explain why these comparisons are made in section 1 of this release (‘Comparisons with the same period a year earlier’).

LTT statistics by time period and transaction type on StatsWales

LTT statistics on total tax due including transactions with restricted detail on StatsWales

By the close of 15 June 2020, the total tax due for April 2019 to March 2020 was £265 million.

Untypically large transactions

‘Untypically large transactions’ in 2019-20 entirely consists of a small number of public sector transactions. These transactions relate to Transport for Wales’ purchase from Network Rail of the Core Valley Line rail asset in Wales. Details of these transactions are presented here to aid transparency of this large public sector transaction, with agreement of the buyer (Transport for Wales) and seller (Network Rail). Further information on these transactions is available from the Transport for Wales website.

Transactions with restricted detail (to protect confidentiality)

For some transactions, we are unable to provide any information other than the total tax due figure in the year, as there is a risk of revealing details of the individual transactions. These are rounded to the nearest million pounds for additional protection. They should only be included if seeking a value for total LTT revenue in the year.

Annual comparisons on a like-for-like basis

However, excluding these transactions, the total tax due for April 2019 to March 2020 was £234.4 million. To make comparisons with earlier periods and by transaction type on a like-for-like basis, it is this value we use (see Figure 2.3).

Despite a small fall in the number of transactions in April 2019 to March 2020 (compared with the previous year), the total tax due increased by 3% on a like-for-like basis. This is mainly due to:

- upwards movement in residential property values and the associated tax due on each transaction

- an increased number of transactions paying the higher rates of residential tax

For April 2019 to March 2020, £63.9 million of additional revenue was raised from higher rates transactions. This is 8% higher than our equivalent estimate for April 2018 to March 2019 (published in June 2019).

Impact of coronavirus (COVID-19) on these statistics

The coronavirus (COVID-19) crisis has had an impact on these figures (up to March 2020), but it is a minor one. More detail about this is shown in Figure 2.1 in section 2 of this release.

Analysis within Wales

Our annual statistics for April 2019 to March 2020 by local authority show:

- for residential transactions, the average tax due per transaction was highest in Monmouthshire (£6,770). For non-residential transactions, this figure was highest in Cardiff (£29,020).

- for residential transactions, the average property value per transaction was highest in Monmouthshire (£282,200) and lowest in Blaenau Gwent (£102,200).

- higher rates transactions as a percentage of all residential transactions varied between 16% in Torfaen and 38% in Gwynedd.

A number of factors can mean a residential transaction is subject to higher rates. These include:

- purchasing buy-to-let properties

- buying a second home or holiday home

- buying a new property while trying to sell an existing one

- companies like social housing providers buying properties

The LTT statistics only include properties sold in the past year. They don’t represent the full stock of properties in any local authority.

In addition, section 9 of this release analyses LTT statistics by the level of deprivation. This analysis uses the Welsh Index of Multiple Deprivation (WIMD).

Statistician’s comment

Adam Al-Nuaimi, Head of Data Analysis in the WRA, commented on these statistics:

We’re pleased to publish our second annual LTT statistics. We present analysis within Wales, including by local authority, Senedd constituency and by level of deprivation.

Figure 1.1 above shows revised estimates of annual data for April 2019 to March 2020. These show general increases in tax due from a year earlier, despite broadly static numbers of transactions.

Most transactions were received before the coronavirus (COVID-19) outbreak took hold, so any impact on these statistics is minor.

In this release, we also present tax due on transactions effective up to the end of May 2020, and the weekly number of transactions submitted (up to week beginning 27 June).

- Residential tax due in April and May 2020 was less than half of that seen in April and May 2019, respectively.

- Non-residential tax due was steady in April 2020 before falling to its lowest ever level in May 2020.

- The weekly number of transactions submitted to the WRA has gradually risen from the low point in April, up to the end of June – but remains considerably below the long-term average.

We’ll continue to monitor this situation in our data-only releases. We’ll comment in more detail in our next quarterly release for April to June 2020 data, to be published on 30 July.

1. About these statistics

Introduction of LTT

From 1 April 2018, LTT replaced Stamp Duty Land Tax (SDLT) on residential and non-residential property and land interests purchased in Wales. The tax rates and tax bands for LTT vary depending on the type of transaction.

LTT statistics are not fully comparable to previous SDLT statistics. This is because different rates and bands are used in LTT. The reliefs may also be different for the two taxes. For example, first time buyers’ relief applies to SDLT but not to LTT.

Value of LTT statistics

Timely information on activity in the property market is important for policy makers. When filing an LTT return about a property transaction, the organisation paying the return has 30 days after the effective date to submit and pay any tax due. LTT statistics therefore are relatively timely.

Forecasting LTT revenues for Wales in future is an important use of LTT statistics. The Welsh Government and the Office for Budget Responsibility mainly do this.

Data available for LTT

All of the data used in this statistical release is available in a spreadsheet on the headline statistics page.

Alongside this annual release, we publish geographic datasets for LTT on the StatsWales website. This includes annual data by:

- local authority

- Senedd Constituency (for residential transactions only)

- level of deprivation, using the Welsh Index of Multiple Deprivation (for residential transactions only)

- built up areas (for residential transactions only)

We provide links to the relevant StatsWales datasets throughout this release.

Timing of and revisions to LTT statistics

The diagram on the key quality information page explains the timing of LTT statistics. We present provisional estimates for May 2020 and revised estimates for periods before this. We will revise the provisional data in future. Not all tax returns for these periods may yet have been received.

In future, we may continue to revise statistics for earlier periods to account for any amendments to transactions and new tax returns received. In particular, this will be due to:

- higher rate refunds being made for several years after the date of the original transaction

- taxpayers mistakenly sending tax returns to HMRC which relate to Welsh property transactions. Once the error has been realised, it can take some time for the taxpayer to send the return correctly to the WRA.

- paper returns not being collected since the end of March 2020. This is due to coronavirus (COVID-19) and our post room not being accessible. We expect there will be a small number of returns relating to April 2019 to March 2020 which we have not yet received, however we expect these to be low value transactions. There is an incentive for the buyer to submit transactions digitally to obtain the LTT certificate (proof of submission), particularly for larger transactions.

Comparisons with the same period a year earlier

There can be seasonal patterns in the property market, with higher levels of activity generally seen in the summer and autumn, and lower levels in winter and spring. These effects are also seen in the levels of transactions and tax due. Therefore, it can helpful to compare the current period with data for the same period a year earlier.

However, in our monthly and quarterly statistics, we are gradually revising downwards the tax due for earlier periods. This is because of higher rate refunds being paid out in each month (for higher rates residential transactions which were effective in earlier periods, back to April 2018).

The value for April 2018 to March 2019 will have already been subject to some of this downward revision, whereas the equivalent figure for April 2019 to March 2020 will not yet. Also, in future, there will be some upward revisions to the values for April 2019 to March 2020 due to late transactions.

Therefore in this release, we compare:

- April 2019 to March 2020 data against

- our previous estimates for April 2018 to March 2019 (which we published in June 2019)

This provides for the fairest comparisons over time.

Key quality information and glossary pages

Please see the separate glossary and key quality information while reading this statistical release:

- we define relevant terms in the glossary as they are used in this release

- on the key quality information page, we describe how Land Transaction Tax statistics meet the Code of Practice for Statistics and the dimensions of value, trustworthiness and quality

Properties or land sold more than once

These statistics relate to transactions which were effective in particular month, quarter or year. A property or piece of land may have been sold more than once in that time. If so, it would feature multiple times in the statistics.

For example, in 2019-20, our best estimate is that between 4% and 5% of transactions involved a piece of land or property which has been sold more than once in the year.

2. Transactions, tax due and property value taxed

In March 2020, we released an update on publishing WRA statistics due to coronavirus (COVID-19). In this update, we stated that in our future releases for LTT, we would look at any potential impacts of coronavirus (COVID-19) on our statistics.

Weekly number of transactions submitted to the WRA (MS Excel)

Figure 2.1 above shows the total number of transactions submitted to the WRA in each 7-day period. For example, the bar ’27.6’ shows the number of residential and non-residential transactions submitted to the WRA from 27 June to 3 July 2020 (inclusive).

The grey dashed line shows the average weekly number of transactions submitted between January and December 2019 (residential plus non-residential transactions).

Please note that Figure 2.1 shows data by submitted date. This differs from effective date, which is the date that drives most of the analysis in this release.

Figure 2.1 shows the large peak in transactions submitted in the last working week before Christmas 2019. Then the number of transactions submitted drops to a much lower level in the two-week period for Christmas holidays, in line with the previous year.

Weekly transactions submitted in January to March 2020 were around the expected levels based on the early part of the previous year. However, the weekly number of transactions submitted dropped sharply in April following the coronavirus outbreak, particularly in the residential sector.

This drop in the number of transactions received relates in small part to transactions that would have been effective in March. Hence there is a small impact on the revenues shown up to March 2020. However, the main impact of the decline is a reduction in transactions that would otherwise have been effective in April 2020 onwards.

The weekly number of transactions submitted rose gradually throughout May and June 2020, but remains below the levels seen in January to March 2020.

LTT statistics by time period and transaction type on StatsWales

By the close of 15 June 2020, we received details of 61,280 notifiable transactions with an effective date in April 2019 to March 2020. This is 1% lower than our estimate for April 2018 to March 2019 (made in June 2019).

In April 2019 to March 2020, 90% of transactions were residential and 10% were non-residential. These are similar percentages to previous periods.

LTT statistics by time period and transaction type on StatsWales

LTT statistics on total tax due including transactions with restricted detail on StatsWales

By the close of 15 June 2020, the total tax due for April 2019 to March 2020 was £265 million (shown in Figure 1.1).

‘Untypically large transactions’ in 2019-20 entirely consists of a small number of public sector transactions. These transactions relate to Transport for Wales’ purchase from Network Rail of the Core Valley Line rail asset in Wales. Details of these transactions are presented here to aid transparency of this large public sector transaction, with agreement of the buyer (Transport for Wales) and seller (Network Rail). Further information on these transactions is available from the Transport for Wales website.

In addition, for some transactions we are unable to provide any information other than the total tax due figure in the year, as there is a risk of revealing details of the individual transactions. These are rounded to the nearest million pounds for additional protection.

The untypically large transactions and transactions with restricted detail should only be included if seeking a value for total LTT revenue in the year.

However, excluding these transactions, the total tax due for transactions with an effective date in April 2019 to March 2020 was £234.4 million. To make comparisons with earlier periods and by transaction type on a like-for-like basis, it is this value we use (see Figure 2.3).

This value is 3% higher than our estimate for April 2018 to March 2019 (published in June 2019). The corresponding changes for residential tax due and non-residential tax due were a 7% increase and a 6% fall, respectively.

LTT statistics by time period and transaction type on StatsWales

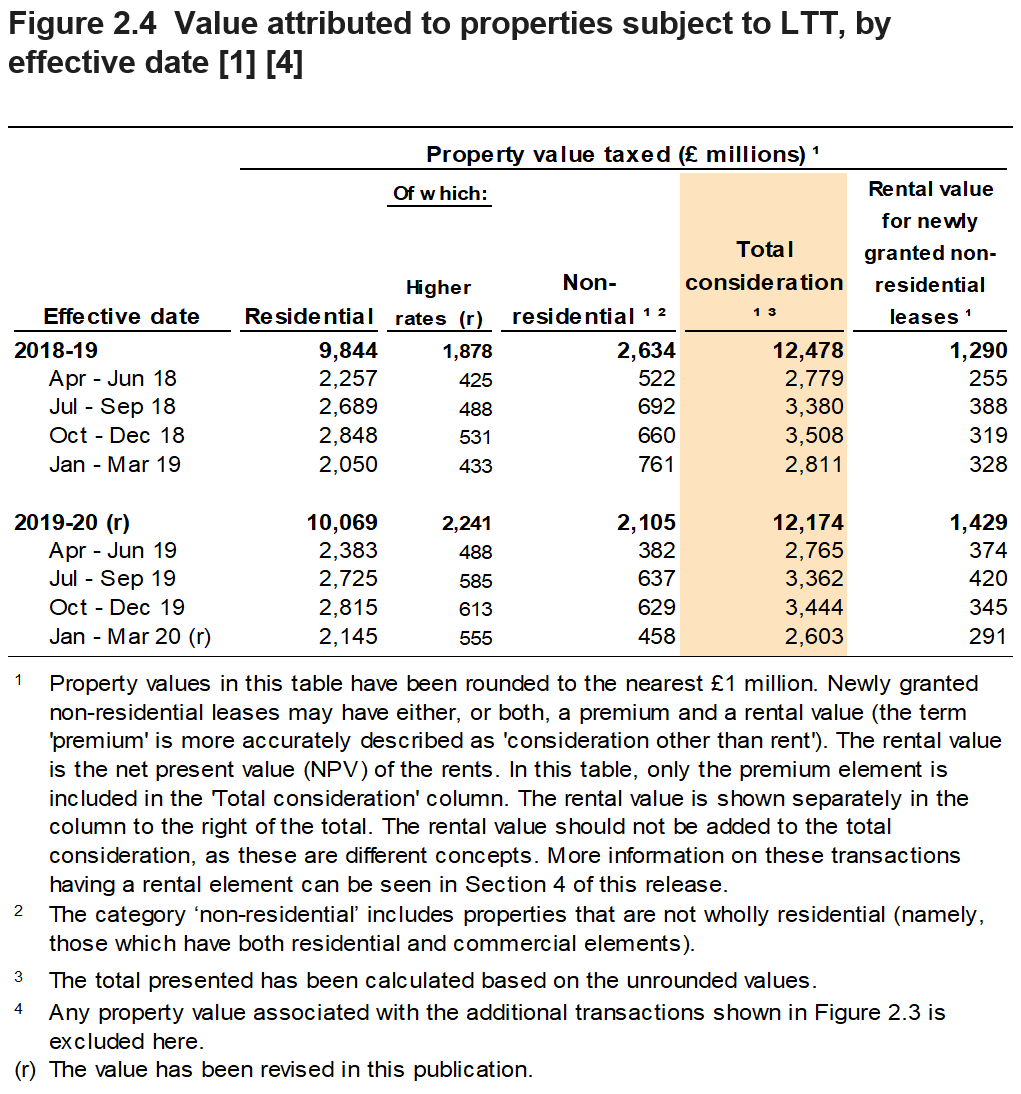

The value of property taxed in the year April 2019 to March 2020 was £12.2 billion.

Separately, the rental value for newly granted non-residential leases was £1.4 billion in the year April 2019 to March 2020.

LTT statistics by time period and transaction type on StatsWales

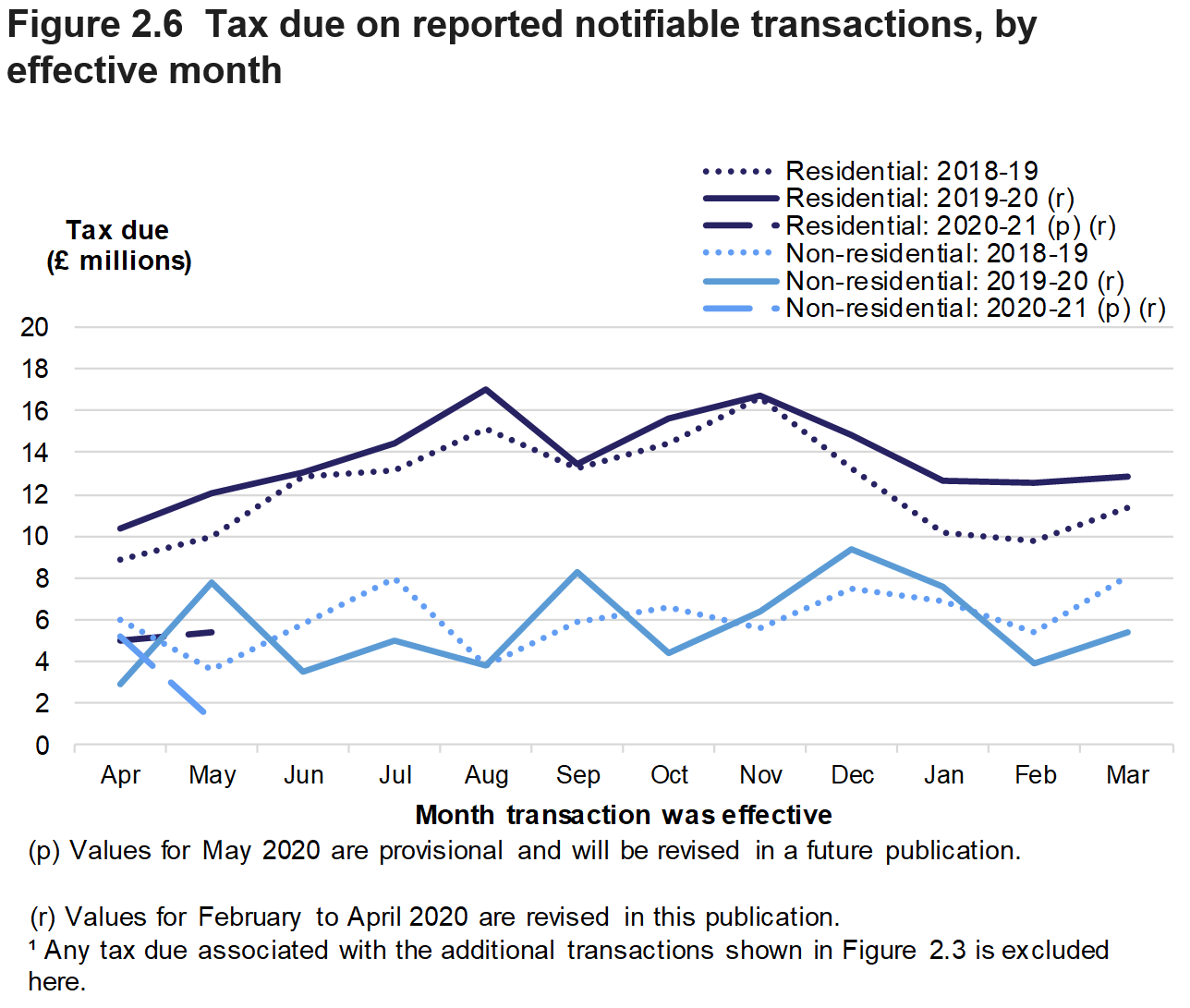

The numbers of residential transactions by effective month has varied greatly since April 2018. The monthly trend in residential transactions in 2019-20 has broadly tracked that of the previous year. There are some differing peaks between years, in some cases due to there being five Fridays in certain months, rather than four. Figure 2.9 in this release shows that nearly half of transactions have an effective date that is a Friday.

In March, we see an increase from the previous month (February) in non-residential transactions. This may be expected, as it is common for non-residential leases to be renewed at the end of the financial year.

As commented below Figure 2.1, coronavirus (COVID-19) has led to a large reduction in the number of residential and non-residential transactions at the start of the 2020-21 year.

LTT statistics by time period and transaction type on StatsWales

As may be expected, similar trends are seen in the monthly tax due as are seen in the monthly counts of transactions. However, the generally higher revenues for residential transactions in 2019-20 can be partly explained by higher rates refunds that have yet to be claimed for 2019-20 transactions. Figure 1.1 presents numbers which better takes account of this effect.

There is greater volatility in the monthly series for non-residential transactions. They also make up a larger share of total tax due than the share of the number of transactions.

As commented below Figure 2.1, coronavirus (COVID-19) has led to a large reduction in revenues at the start of the 2020-21 year. Residential revenues in April and May 2020 were less than half of the revenues in these months a year earlier. Non-residential revenues were steady in April 2020 before falling to the lowest level seen to date in May 2020 (£1.2 million).

LTT statistics by transaction type and transaction description on StatsWales

The value of the properties associated with conveyances and transfer of ownership during April 2019 to March 2020 was £11.6 billion (not shown in Figure 2.7).

Most transactions in April 2019 to March 2020 were associated with a conveyance or a transfer of ownership. This figure was 94% for residential transactions and 66% for non-residential transactions.

A new lease was granted in 31% of non-residential transactions (compared with 2% of residential transactions).

Similar percentages are seen for the previous year and by quarter.

Analysis by submission date of the return

We are aware that some other statistical publications in the UK base their analysis on the date that the tax return is submitted. We have therefore produced some comparable figures to other UK countries (using date submitted) and compared these to our effective date statistics.

As might be expected, the monthly trend is generally quite similar for the monthly series of transactions submitted and transactions by effective date. The largest differences between the two numbers were seen in the following months:

- in April 2018, 1,360 more transactions were effective than were submitted. This is largely because there were no LTT transactions which would have been effective in March 2018 to act as a balance for those effective in April that were received in May 2018. These March 2018 transactions were still being submitted to HMRC under the predecessor tax regime of Stamp Duty Land Tax.

- in the months December and January, differences of up to 600 transactions can be seen. This is likely due to Christmas holidays and delays in submitting transactions around this time.

Friday was the most popular day for both transactions to be submitted and for transactions to become effective, with very few on a weekend. This reflects the typical working week of agents who complete LTT returns.

Nearly half of transactions effective in April 2019 to March 2020 became effective on a Friday. While an above average proportion of returns were submitted on a Friday, the difference is far less pronounced than for effective date. This suggests that returns are generally not submitted on the same day that the transaction completes.

Although not shown above, there is also evidence within the data of even more marked peaks in submissions on the last Friday of each month.

3. Residential transactions by value

Please note that all analyses in section 3 exclude the additional transactions which were untypically large and those with restricted detail (shown in Figure 1.1 in the ‘Main points’ section of this release).

LTT statistics by time period and residential transaction value on StatsWales

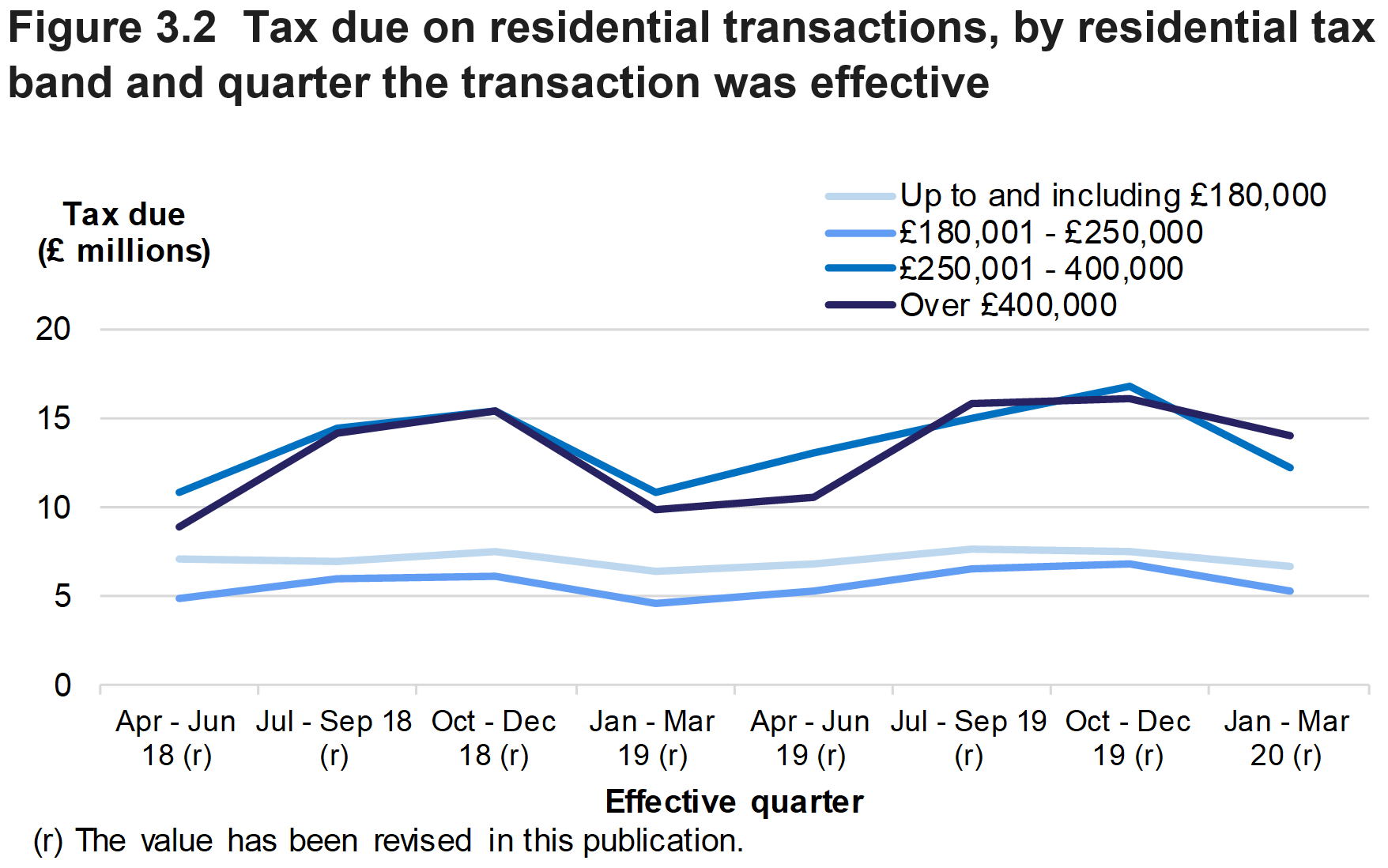

For each tax band, Figures 3.1 and 3.2 show the quarterly trends in the number of residential transactions and tax due. There are six residential tax bands. We have combined the largest three bands here to show results for properties purchased for more than £400,000.

Similar seasonal trends for the tax bands can be seen in both numbers of transactions and tax due. Most of the tax bands show a fall in transactions and tax due in January to March (compared with the preceding October to December).

However, there is greater volatility in the trends when considering the tax due on properties in the higher value bands. For properties purchased for more than £400,000, the tax due in October to December 2019 was the highest quarterly value seen to date. This was also the case for properties purchased for between £250,000 and £400,000.

LTT statistics by time period and residential transaction value on StatsWales

In the year April 2019 to March 2020, just over three fifths of residential transactions were within the first tax band (purchase price £180,000 or lower). Although the main tax rate on residential transactions of up to £180,000 is 0%, these transactions still accounted for around a sixth of total residential tax due, which relates to the higher rates residential component of the tax.

Combining the fourth, fifth and sixth bands (purchase price of greater than £400,000), these accounted for only 4% of transactions. However, the tax due for these transactions accounted for 34% of the total residential tax due.

4. Non-residential transactions by value

Please note that all analyses in section 4 exclude the additional transactions which were untypically large and those with restricted detail (shown in Figure 1.1 in the ‘Main points’ section of this release).

LTT statistics by time period and non-residential transaction value on StatsWales

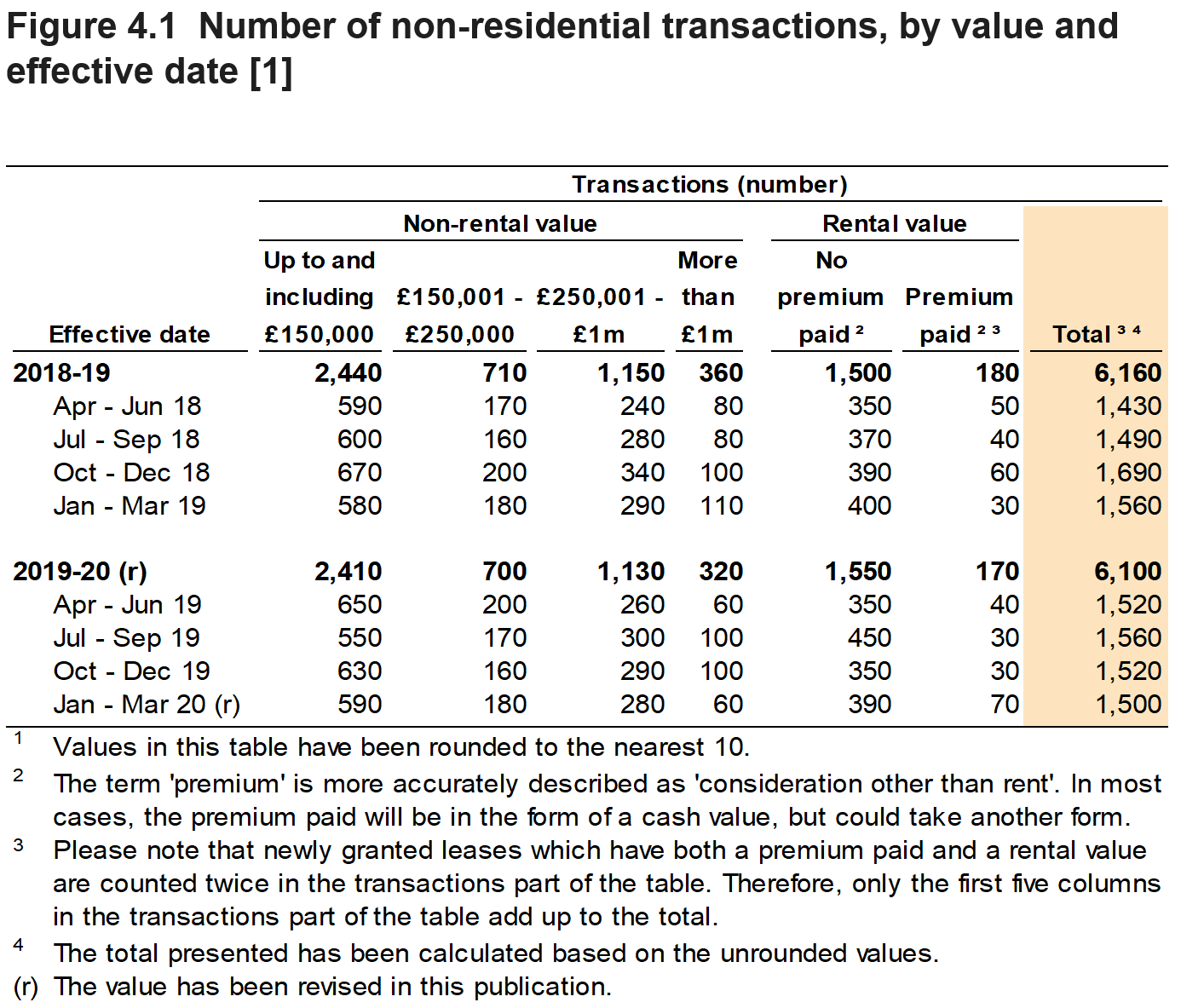

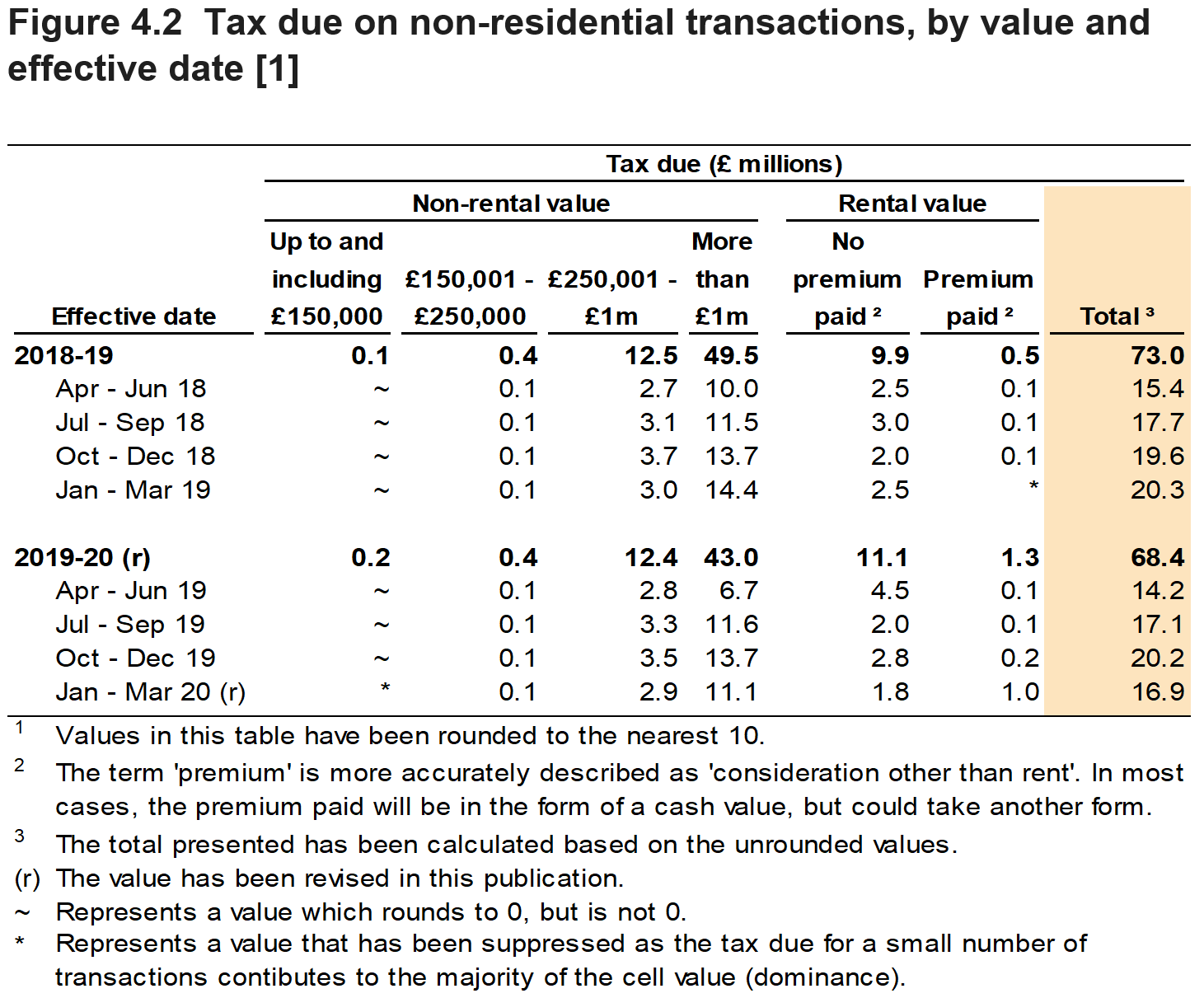

Figures 4.1 and 4.2 show that there were 6,100 non-residential transactions effective in April 2019 to March 2020 with £68.4 million tax due.

In each three-month period since April 2018, around 50% to 70% of the tax due has been contributed by transactions with a non-rental value greater than £1 million. In each three-month period, around 10% to 30% of the tax due has been contributed by the rental value of non-residential properties.

LTT statistics by time period and non-residential transaction value on StatsWales

Figure 4.3 shows that in April 2019 to March 2020, 5% of non-residential transactions had a non-rental value of more than £1 million. These transactions accounted for 63% of the non-residential tax due (Figure 4.4).

Figure 4.3 also shows that for 28% of non-residential transactions in this period, a rental value was associated with the property (which contributed to the tax paid on the transaction).

The rental value of non-residential properties accounted for 18% of the total non-residential tax due (Figure 4.4).

5. Reliefs

Please note that all analyses in section 5 exclude the additional transactions which were untypically large and those with restricted detail (shown in Figure 1.1 in the ‘Main points’ section of this release).

Taxpayers can claim reliefs on both residential and non-residential transactions. Reliefs reduce the amount of tax due when certain conditions are met. More than one relief can be applied to a single transaction.

Reliefs may reduce the tax due:

- to zero, known as a full relief

- or by a certain percentage or amount, known as a partial relief

LTT statistics on reliefs by measure and transaction type on StatsWales

There were 1,520 transactions in April 2019 to March 2020 with reliefs applied to them that reduced the associated tax due. This is higher than the previous year.

On average, there are around 130 reliefs claimed in each three-month period which had no impact on the tax due. These reliefs are excluded from Figure 5.1. Many of them have been reported unnecessarily by the organisations completing the tax return. As an example, some of these apply to low value residential transactions. Indications are that they are due to a perceived but mistaken need to claim first time buyer relief (which applies for the predecessor tax, but not to LTT). This is known following queries raised with several agents asking why tax reliefs have been claimed where there is no impact on value of the tax. Further information about this category of reliefs is provided in Example 4 in our key quality information.

This example also describes some adjustments that have been made to more correctly identify the value of tax relieved associated with these transactions. We expect further adjustments in future and we therefore expect to revise Figure 5.1 in future.

Prior to April 2020, we excluded linked and relieved transactions from Figures 5.1 and 5.2 in our releases. This was so that we could carry out further analysis on these transactions. We have now carried out this analysis and have a reasonable level of confidence in the quality of these data. In our quarterly release published in April 2020, we added linked and relieved transactions into Figures 5.1 and 5.2, revising all data back to April 2018. This has added:

- around 60 to 70 transactions each quarter into Figure 5.1

- an average of £4 million to £5 million each quarter into Figure 5.2

LTT statistics on reliefs by measure and transaction type on StatsWales

For each three-month period, the numbers of reliefs claimed on residential transactions was higher than for non-residential transactions. However, in most of the three-month periods, non-residential transactions contributed around 70% to 90% of the total value of reliefs claimed. The value of reliefs claimed in each three-month has varied considerably over time.

In this release, we have corrected downwards the value of reliefs claimed on some transactions. For example, residential reliefs in January to March 2020 have been revised downwards from £8.4 million (as published in April 2020) to £3.2 million in this release. This is due to us discovering that the consideration on some transactions was 100 times higher than it should have been, and correcting those errors. Further information on this is provided in Example 6 in our key quality information.

LTT statistics on reliefs by measure and transaction type on StatsWales

The type of relief with the largest impact on tax due in April 2019 to March 2020 was group relief, predominantly in non-residential transactions. This relief accounted for just over half of the total tax relieved.

In April 2019 to March 2020, the total value of reliefs claimed was £50.6 million. This is lower than the £69.9 million claimed in April 2018 to March 2019.

6. Higher rate refunds

LTT statistics on higher rate refunds by original transaction date on StatsWales

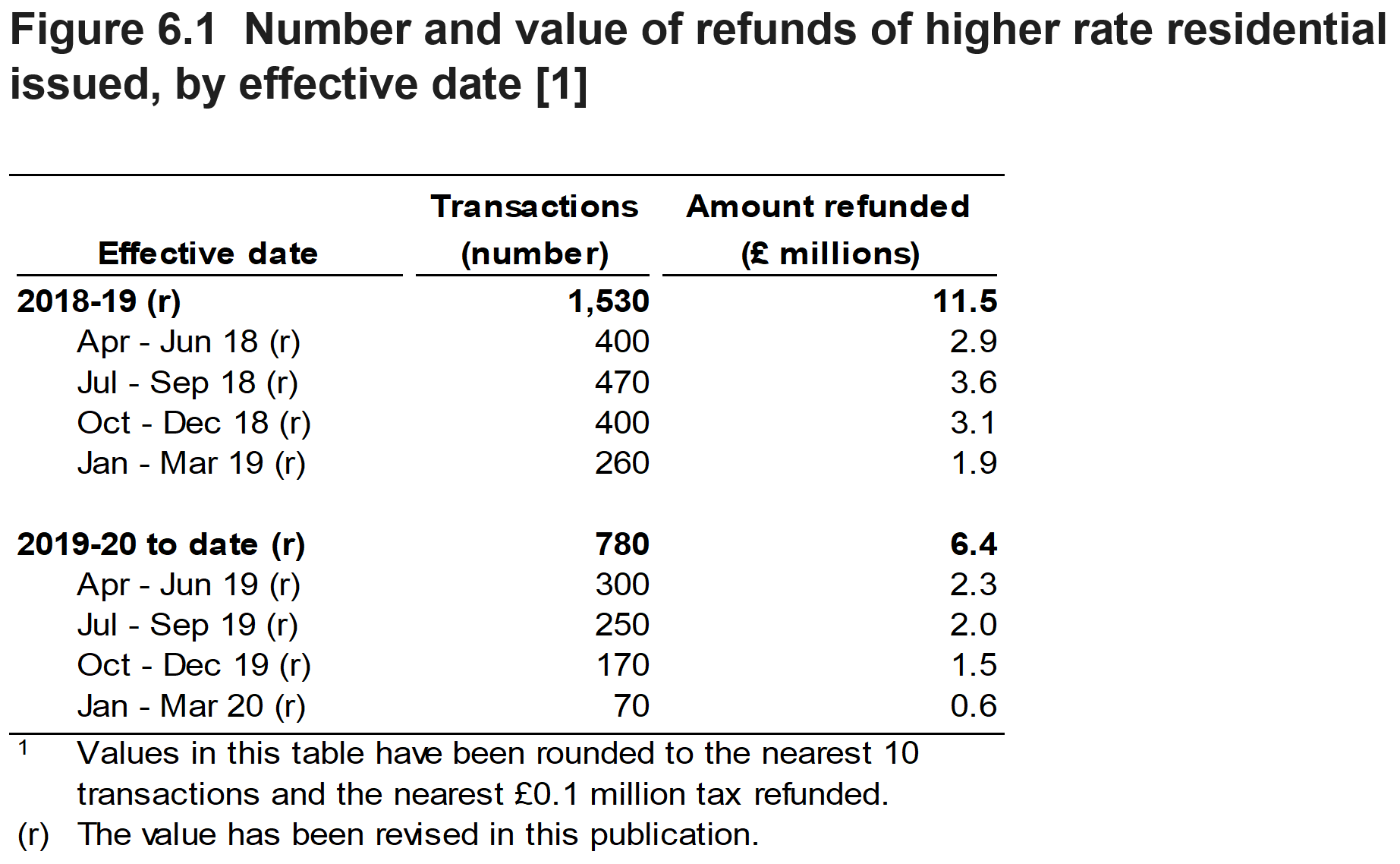

When a taxpayer claims a refund for higher rates residential LTT, the original transaction is amended to a main rate residential LTT transaction. The data in this release is adjusted for any refunds approved by WRA up to and including 15 June 2020.

Figure 6.1 shows that 780 higher rate refunds were claimed for transactions effective in April 2019 to March 2020, with £6.4 million refunded to taxpayers.

Taxpayers have up to three years to sell their previous main residence and claim a refund. Therefore, all the values in Figure 6.1 will continue to be revised upwards in future editions of our statistics. This will also to lead to the total tax due in other tables and charts reducing.

The number and value of refunds presented for January to March 2020 are lower than for earlier periods. This is because compared with earlier periods, not enough time has passed since the transaction was effective for many of the relevant taxpayers to sell their previous main residence and claim their refund.

Refunds of higher rates residential by date the refund was approved

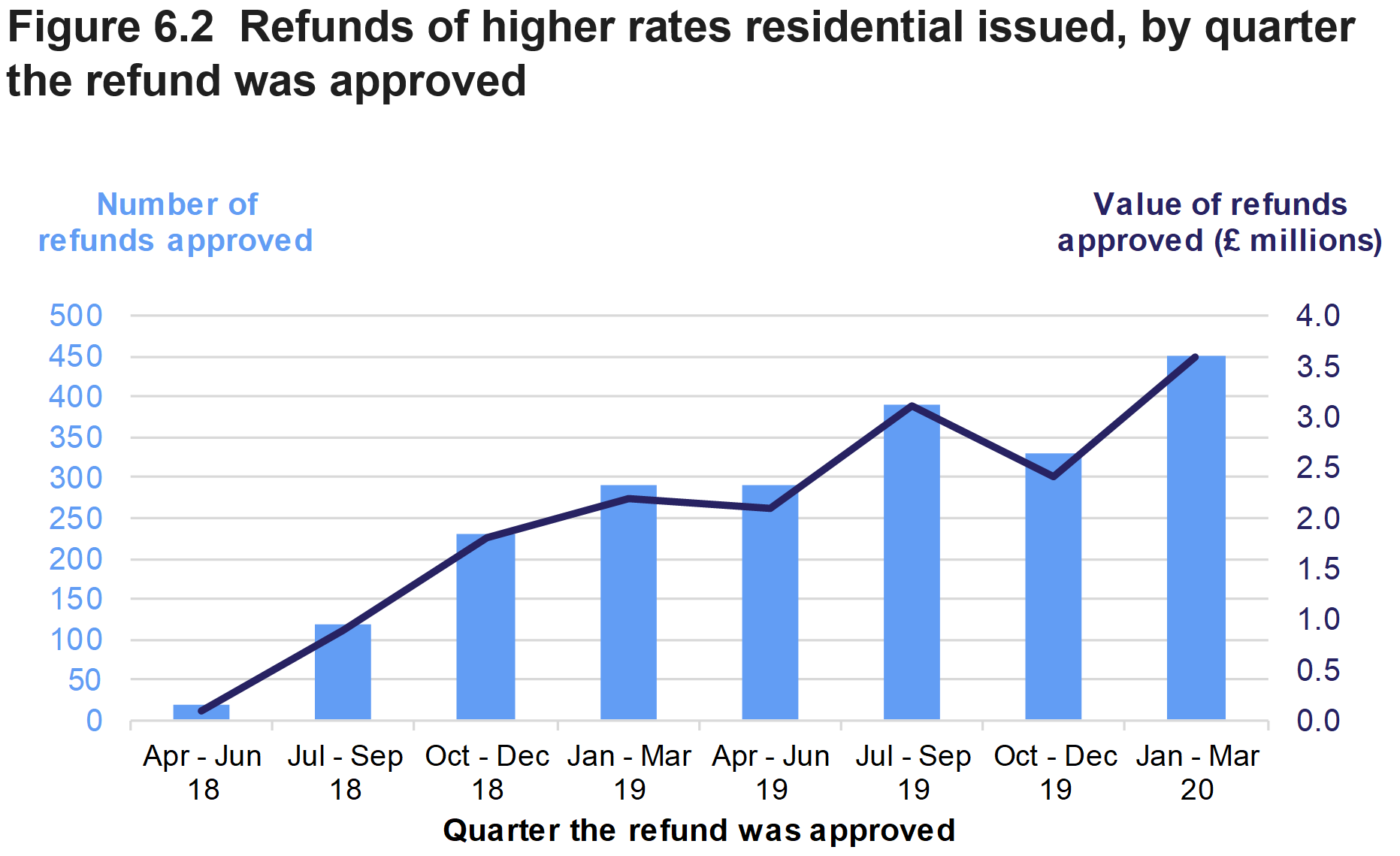

Figure 6.2 below shows another useful way of presenting data on higher rates refunds, using the date when the refund was approved by the WRA.

The number of refunds approved (and value of those refunds) increased in most quarters during April 2019 to March 2020. This reflects expectations as sufficient time has passed for claims to be made.

There has been a fall in the data for October to December 2019. This is likely to be due to:

- lower numbers of transactions during autumn and winter (than spring or summer).

- changes to processes in the WRA operations team during October to December 2019. This led to catching up on the processing of refunds in early 2020.

Refunds of higher rates residential (cash basis)

Further information on the refund payments made to taxpayers, by the month in which they were made, can be found at the link below.

LTT statistics on tax paid and higher rate refunds (cash basis) on StatsWales

In the main, these additional data are provided to support forecasting requirements.

Intention to claim a refund of the higher rates element

For all higher rates transactions, the WRA asks the question whether the taxpayer intends to reclaim the higher rates element in future. It will take several years before we know how likely someone is to claim based on their stated intentions (it can take up to three years to make the claim). But we do currently know that around 70% of those who do claim answer this question in the positive.

7. Tax paid

LTT statistics on tax paid and higher rate refunds (cash basis) on StatsWales

In April 2019 to March 2020, the WRA received £232.9 million in LTT payments. This value has been revised down slightly (from £233.5 million) presented in our April 2020 release. This is due to removing some double-counting of payments from the data.

These figures are less than those reported in Figure 2.3 as they relate to the payments received in each month (often referred to as ‘on a cash basis’). This differs from earlier tables in this release which are based on transactions that were effective in the month.

There is a difference in April 2018 as the WRA only started collecting the tax in that month. Therefore, no payments relating to transactions effective in earlier months were relevant.

Excluding the core valley lines transaction, the highest monthly receipts seen to date were in December 2019 (£30.5 million).

WRA accounts

LTT transactions are subject to revision for various reasons, for example following a review into their accuracy, or the granting of higher rates refunds. As the data in this release is largely based on the effective date of the transaction, which usually remains the same, then much of the data published here for previous periods can still change.

Whilst virtually all the transactions relating to 2019-20 should now be included in this release (due to the time that has elapsed since the end of the year), data for 2018-19 and 2019-20 will never be fully finalised until the window for revisions closes. In the case of higher rate refunds this can be as much as three years after the original transaction, with a potentially longer window available for certain other transactions, such as those which WRA choose to open an enquiry into.

For the purposes of accounting and forecasting, it is necessary to create a final figure at the Wales level for the total tax due for each year. Whilst the value of the money received in figure 7.1 is fixed as soon as each period ends, this is too simplistic for this purpose. For example, Figure 7.1 doesn’t identify the tax year to which each transaction relates.

Instead a final accounting figure for 2019-20 is defined by including transactions (or any amendments to transactions) received up until 30 April 2020 with an effective date in 2019-20. Any transactions received (or amendments made) since 30 April 2020, or yet to be received are excluded. This data has been formally published as part of the WRA’s accounts for 2019-20, as laid before the Welsh Parliament.

|

Transaction type |

2018-19 |

2019-20 |

|

|---|---|---|---|

|

Residential |

155.4 |

163.4 |

|

|

Non-residential |

72.4 |

96.9 |

|

|

Total |

227.8 |

260.3 |

|

A key difference between the total revenue for 2019-20 (Figure 7.2) and our wider statistics relates to higher rate refunds. Transactions refunded during 2019-20 (which relate to an original transaction in 2018-19) will act on the 2019-20 value in Figure 7.2, but on 2018-19 values in our wider statistics.

8. Analysis within Wales

Please note that all analyses in section 8 exclude the additional transactions which were untypically large and those with restricted detail (shown in Figure 1.1 in the ‘Main points’ section of this release).

Data by local authority

This release presents geographic breakdowns for LTT (on an annual basis only). We have not provided breakdowns by month or quarter, as there would be too few transactions in most local authorities to provide reliable statistics.

The local authority in which the transaction occurs is a mandatory question on the tax return, whereas the postcode where the transaction occurs is an optional question. We have combined these two pieces of information to derive our local authority statistics. Further information on this process and the data quality is available in our key quality information for LTT statistics.

We present local authority data for residential and non-residential transactions and tax due.

We present local authority data on the value of properties taxed (known as the consideration) for residential transactions only. This is because there are some non-residential transactions with a particularly large consideration and a possible risk of identifying a taxpayer if we were to publish annual local authority data on these.

In future, we will investigate the viability of combining several years of non-residential transactions to support safe publication of consideration data.

Data by Senedd constituency and built up area

We also publish annual statistics for Senedd constituencies and built up areas. These statistics are not analysed in this release but are available on the StatsWales website. These statistics are published for residential transactions only.

Where supplied, the postcode on the tax return is used to derive the Senedd constituency.

Where the postcode is not supplied, there is a clear bias towards larger non-residential transactions, and as these cannot be allocated to a Senedd constituency area, the resulting statistics are not reliable. Therefore, it is not currently appropriate to produce statistics on non-residential transactions for Senedd constituencies and built up areas.

Presentation of averages in this section

Where Wales averages are presented in this section, these are a weighted mean which takes account of different numbers of transactions in each local authority.

Figures 8.1 to 8.4 present ratios (for example tax due per transaction or higher rates transactions as a proportion of all transactions), This use of ratios is needed to create comparable data across all local authorities, as the individual concepts will often vary greatly between local authorities simply due to their varying size and population.

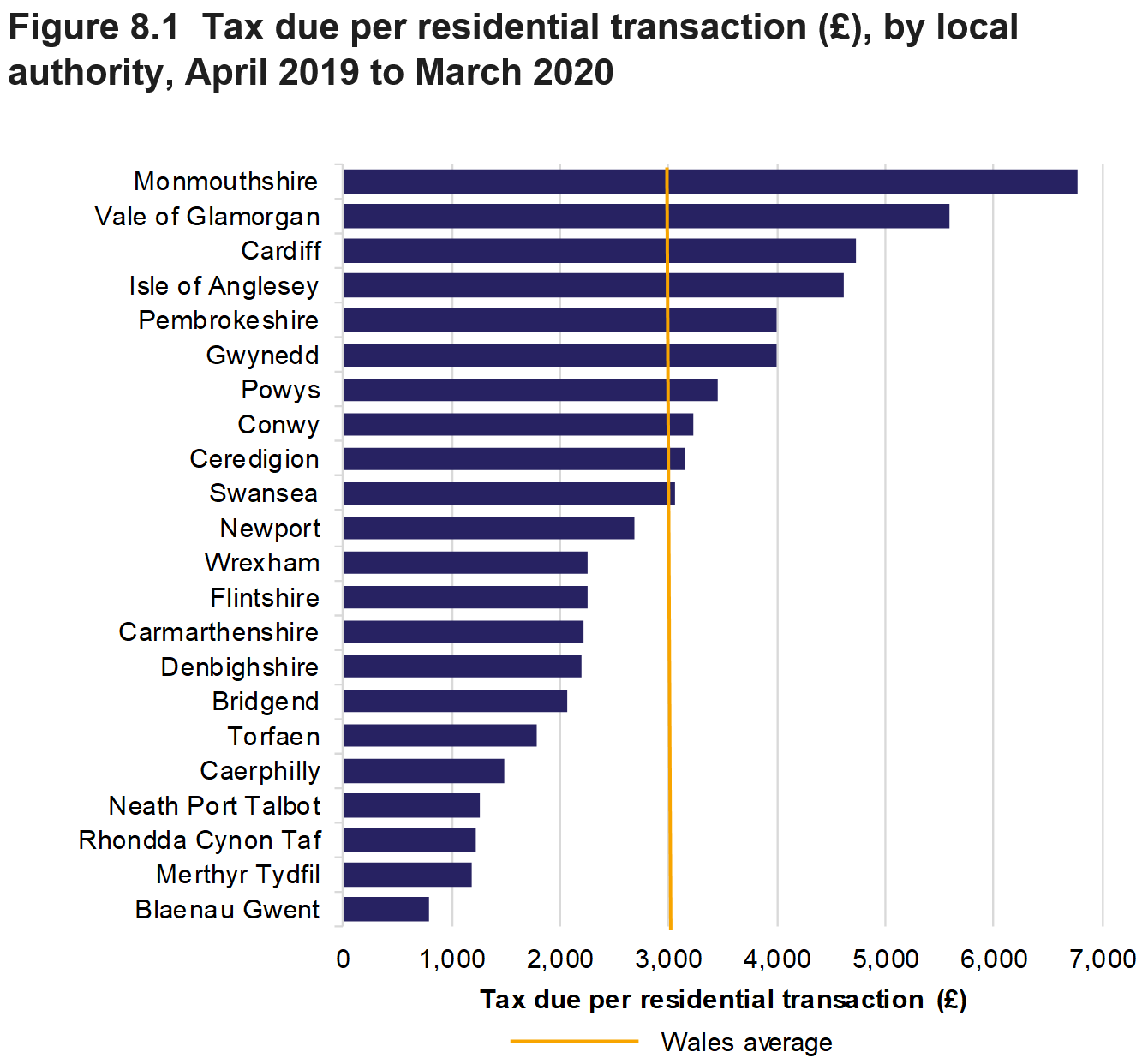

As an example, consider Figure 8.1. Among Welsh local authorities, Cardiff had both the highest amount of residential tax due and number of residential transactions. Due to their size, this would prevent meaningful comparison across local authorities, but when looking at tax due per residential transaction, a much smaller authority (Monmouthshire) exhibited the highest figure, with the comparable figure in Cardiff being the third largest.

Residential LTT statistics by measure and local authority on StatsWales

Figure 8.1 shows that for residential transactions, the average tax due per transaction was highest in Monmouthshire (£6,770) and Vale of Glamorgan (£5,580).

The average tax due per residential transaction was lowest in Blaenau Gwent (£800) and Merthyr Tydfil (£1,180).

For April 2019 to March 2020, the ordering and distribution of local authorities in this chart is very similar to the previous year.

Non-residential LTT statistics by measure and local authority on StatsWales

Figure 8.2 shows that for non-residential transactions, the average tax due per transaction was highest in Cardiff (£29,020).

The average tax due per non-residential transactions was lowest in Blaenau Gwent (£1,260).

As with residential transactions, the tax due for individual transactions in a local authority varied widely around the average figure for Wales.

Although the patterns seen for residential and non-residential are quite similar, there are some clear differences in the ordering of the local authorities between the two charts.

For April 2019 to March 2020, the relative position in the chart for some local authorities has changed considerably (compared with April 2018 to March 2019). For example, Caerphilly has risen from 17th highest to 2nd highest, while Monmouthshire has fallen from 3rd highest to 10th highest. This illustrates the volatility in the non-residential data from year to year.

Residential LTT statistics by measure and local authority on StatsWales

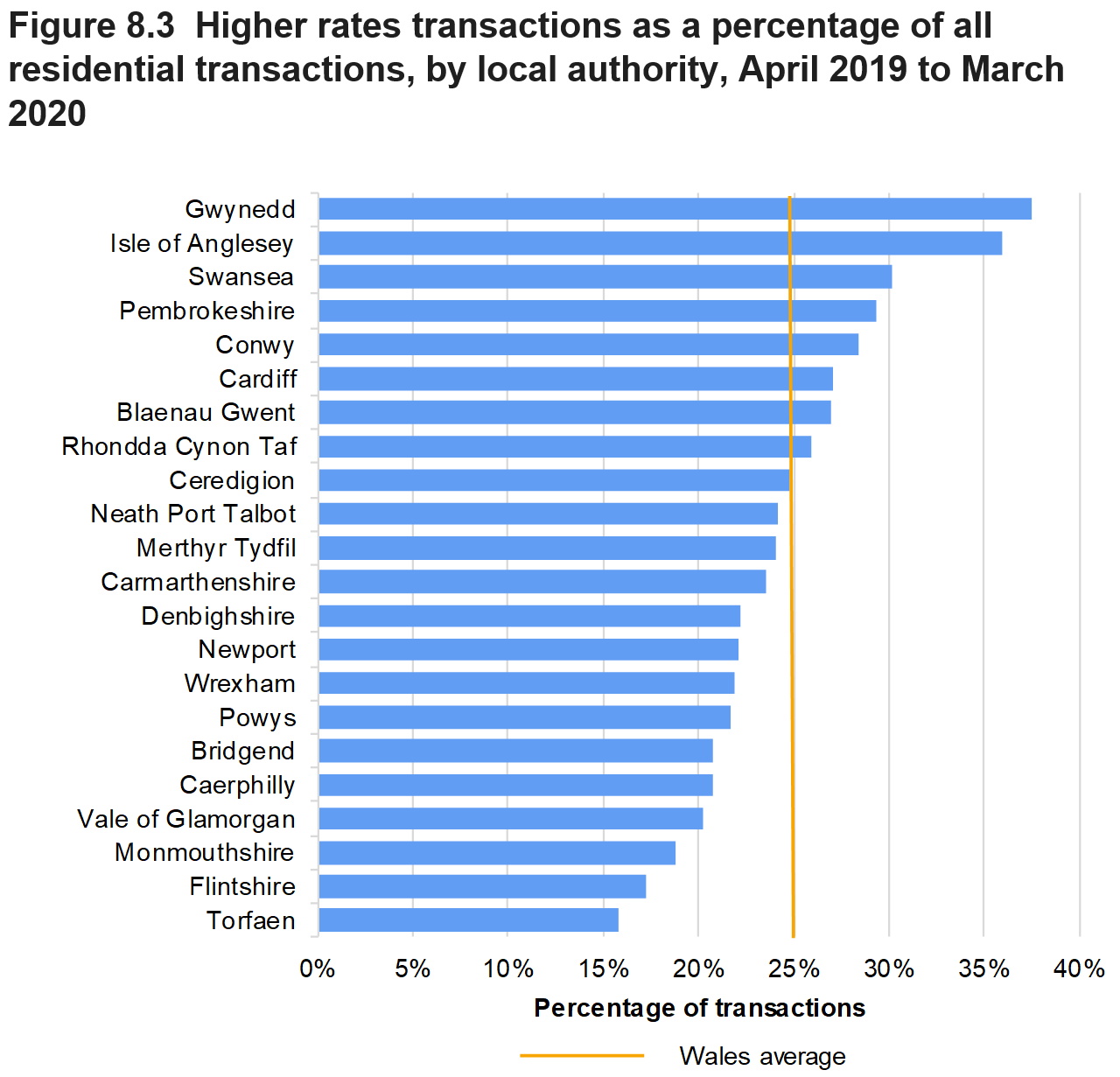

Figure 8.3 shows the wide variation between local authorities in the level of higher rates residential transactions. This data is presented as a percentage of all residential transactions.

Higher rates transactions were generally more common in authorities located in the northern and western parts of Wales. The highest percentages were seen in Gwynedd (38%), Isle of Anglesey (36%) and Swansea (30%).

The lowest percentages were seen in Torfaen (16%) and Flintshire (17%).

For April 2019 to March 2020, the ordering and distribution of local authorities in this chart is similar to the previous year.

Residential LTT statistics by measure and local authority on StatsWales

For residential transactions, the highest average property value per transaction was in Monmouthshire (£282,200) and Vale of Glamorgan (£249,900), and lowest in Blaenau Gwent (£102,200) and Merthyr Tydfil (£123,100).

For April 2019 to March 2020, the ordering and distribution of local authorities in this chart is very similar to the previous year.

9. Analysis by Welsh Index of Multiple Deprivation area

Please note that all analyses in section 9 exclude the additional transactions which were untypically large and those with restricted detail (shown in Figure 1.1 in the ‘Main points’ section of this release).

In this section of the release, we analyse LTT for Welsh Index of Multiple Deprivation (WIMD) areas. This analysis shows the level of transactions and tax due in the most and least deprived areas of Wales.

These statistics for WIMD areas are published for residential transactions only. Where supplied, the postcode on the tax return is used to derive the WIMD area. Where the postcode is not supplied, there is a clear bias towards larger non-residential transactions, and as these cannot be allocated to a WIMD area, the resulting statistics are not reliable. Therefore, it is not currently appropriate to produce statistics on non-residential transactions for WIMD areas.

What is WIMD and how are we using it?

WIMD is designed to identify the small areas of Wales that are the most deprived. WIMD is currently made up of eight separate domains (or types) of deprivation. Each domain is compiled from a range of different indicators. The eight domains are income, employment, health, education, access to services, community safety, physical environment, and housing. Further information is available on the WIMD webpage.

Where provided, we have linked the postcode from the tax return to around 1,900 small areas in Wales. These small areas are ranked by WIMD from the most to least deprived. These areas are grouped into ten equal sized bands from the most to least deprived (known as ‘deciles’ or ‘tenths’).

WIMD ranks were updated recently (2019). We have used these latest WIMD ranks in this release. Each update of WIMD ranks is designed to last for around three to six years. When we first published this analysis last year, we used 2014 WIMD ranks.

Where averages are presented in this section, this is a weighted mean which takes account of different numbers of transactions in each WIMD tenth.

Furthermore, most of the variation in terms of deprivation is found in the most deprived tenths. The difference (in relative deprivation) between the most deprived and second most deprived tenths is greater than that at the other end of the distribution.

Residential LTT statistics by measure and deprivation area on StatsWales

Because each of these tenths are of a similar size in terms of population, we can analyse the data without scaling for their size, as was necessary for local authorities (see the green box in section 8 of this release). This allows us to consider the number of transactions and tax due separately rather than the ratio between the two items that we analysed for local authorities.

Figure 9.2 shows, as might be expected, that the total residential tax due grows considerably and quite uniformly through the range of areas (from most deprived to least deprived). This represents likely differences in the value of property in these areas.

However, Figure 9.1 also shows that the number of residential transactions is lowest in the most deprived areas of Wales, peaking towards the middle and latter part of the distribution, and dropping down a little for the least deprived tenth. This suggests that deprivation is not only linked to prices but also to the level of activity in the housing market in Wales.

The additional revenue from higher rates also generally grows from the most deprived areas to the latter end of the distribution, before dropping in the least deprived tenth.

For April 2019 to March 2020 LTT data (using 2019 WIMD ranks), the pattern seen in Figures 7.1 and 7.2 is broadly similar to the analysis last year of April 2018 to March 2019 data (using 2014 WIMD ranks).

Residential LTT statistics by deprivation area and transaction type on StatsWales

Figure 9.3 shows the percentage of higher rates transactions within total residential transactions for each WIMD tenth. The proportion of residential transactions which are taxed at the higher rates generally falls from the most deprived areas to the least deprived areas (with some exceptions).

The trend in the percentages (going from most deprived to least deprived) is smoother on this chart than the analysis published last year for April 2018 to March 2019 (using 2014 WIMD data). This is likely to be due to greater alignment between the date of the transactions and the date that applies to the WIMD analysis (2019).

As stated in section 8 of this release, there are various reasons for the higher rates tax being chargeable, two of these being purchases of buy-to-let properties and purchase of second or holiday homes. Figure 9.3, taken together with Figure 9.1 (which shows that the number of higher rates transactions varies only very little between WIMD tenths), may give some insight into the balance between these two items.

Assuming that buy-to-let properties are more likely to be bought in more deprived areas, while second or holiday homes are more likely to be bought further up the distribution, then a tentative conclusion can be drawn that buy-to-let properties are at least as prevalent as second or holiday homes as a factor on why the higher rates of tax are charged. It is therefore important not to assume that any single factor is the driver for the higher rate charge.

Annex A: Analysis of revisions

We look here at the effect of the regular revisions made to Land Transaction Tax statistics. We analyse the differences between the first, second and third estimates published for a month. This is for both the number of transactions and the tax due.

For example, we have published three estimates for March 2020. We published the first estimate on 30 April, published the second estimate on 22 May and the third estimate on 19 June.

Figure A1 shows that higher levels of revisions can generally be seen in the earlier months that the WRA began collecting LTT. This is particularly the case for the tax due for transactions with an effective date in April 2018, where there was a 30% increase in the estimate of tax due (from the first to the second estimate for the month). A larger revision in April 2018 was expected because the familiarity of the system to users would have been lower, and also because an earlier cut-off date in the following month was used to extract the data.

Nevertheless, the 30% figure for April 2018 in terms of tax due is considerably higher than the equivalent figure for the number of transactions (11%). It is explained by a few larger transactions with an effective date late in April 2018 that were not reported to WRA until later in May 2018 (before the 30 day filing limit, but after the cut-off date for the April publication).

Figure A1 also shows the levels of revisions have generally decreased over time. Since October 2018, the revisions between the first and second monthly estimates have generally been between 0 and 3%. Recent exceptions were:

- June 2019 when the tax due was revised up by 9% between the first and second estimate

- September 2019 (tax due was revised upwards by 16%)

- January 2020 (tax due was revised upwards by 27%)

These exceptions are generally due to a small number of larger value returns arriving towards the end of the 30-day notification period.

The lower level of revisions generally seen now is likely to be due in part to an increasing familiarity with the system amongst solicitors and conveyancers completing the returns. It is consistent with a general decrease in the time taken for returns to be filed with the WRA over the same period (not shown in tables or charts).

There may also be seasonal effects in revisions to the data. For example, we saw higher revisions for the July 2018 estimates than the months around it. However, we do not see any obvious seasonal patterns in data for 2019 or so far in 2020. We will require at least another year’s worth of data to properly assess any data seasonality.

We made a downward revision to the non-residential tax due for April 2019 (between the first and second estimates). A non-residential transaction effective in April 2019 was entered incorrectly as being overly large and was later revised.

Revisions between second and third published estimates

In a spreadsheet published alongside this statistical release, Tables A1 and A2 show the difference between first, second and third published estimates for a month.

We see relatively small increases between the second and third estimates for a month. In general, this is also the case for the later estimates for a month (not shown in the tables). However, falls may be seen in the second, third and later estimates of tax due for a month. This is because the data are shown net of any refunds for higher rate residential transactions. These refunds may be claimed several years after the effective date of the original transaction. We analyse refunds in section 6 of this statistical release.

In future, we may consider applying a grossing factor to the first estimates for a month. This may help reduce the revisions required to the first estimate for a month. With the volatility shown in the data to date, it is likely we will need several years of LTT data in order to calculate appropriate grossing factors.

In general, we see larger revisions in the data on non-residential transactions than for residential transactions. This reflects the more volatile nature and often larger size of non-residential transactions.

Links to key quality information and glossary pages

Our key quality information page describes how our Land Transaction Tax statistics meet the Code of Practice for Statistics and the dimensions of value, trustworthiness and quality.

We define relevant terms in the glossary as they are used in this release.

Feedback and contact details

We would be grateful for your feedback on these statistics, to help us improve them. Please contact us using the details below.

Statistician: Dave Jones

Email: data@wra.gov.wales

Rydym yn croesawu galwadau a gohebiaeth yn Gymraeg / We welcome calls and correspondence in Welsh.

Media

Email: news@wra.gov.wales

Rydym yn croesawu galwadau a gohebiaeth yn Gymraeg / We welcome calls and correspondence in Welsh.

![]()