The protocol on Ireland/Northern Ireland: the implications for Wales’ external trade

This note identifies issues that may impinge directly or indirectly on the Welsh economy as a result of the adoption of the Protocol on Ireland/Northern Ireland as part of the Withdrawal Agreement and subsequent Bill.

This file may not be fully accessible.

In this page

Preliminaries

We believe the main implications for Wales from the protocol to be:

- Producers in Great Britain (GB) (including Welsh producers) are likely to lose market share in Northern Ireland (NI) as goods sent from GB to NI will face new customs checks, possibly customs duties, and other regulatory/administrative checks, while NI trade with the EU (notably with the Republic of Ireland - RoI) will remain frictionless.

- If Great Britain relaxes its regulations relative to EU regulations, NI producers might operate under higher costs than GB firms, as NI producers would still need to produce to EU standards. NI firms may therefore struggle to compete in the GB market.

- The more extensive are the trade barriers between the UK and the EU (notably RoI), and the less extensive are the border checks between GB and NI, the more incentive there will be to divert trade from RoI-GB to NI-GB routes. This will likely impact on the level of freight going through Wales to Ireland. The impact might be felt particularly for consignments which are destined for NI but which are currently sent from Wales via RoI.

- Handling whichever new checks are required on trade with the EU will undoubtedly require increased border infrastructure in Welsh ports such as Holyhead, Pembroke Dock and Fishguard. Delays due to border checks will be particularly problematic for perishable food products, which make up a relatively large share of goods shipped between Holyhead and Dublin.

The Protocol on Ireland/Northern Ireland defines the trading arrangements between Great Britain (GB), Northern Ireland (NI), the Republic of Ireland (RoI), the remainder of the European Union (EU) and the rest of the world after the transition period. The objective, in line with the Belfast Treaty (or Good Friday Agreement), is to ensure that there is no border or border formality between NI and RoI. Whereas that is straight forward while the UK and RoI are members of the European Union’s Single Market and Customs Union, once the UK leaves these arrangements it amounts to finding a way of maintaining totally unimpeded commerce between 2 territories with different customs laws and goods regulations. Exiting the Single Market also raises serious questions about the trade in services between the UK and EU, but these are not border issues and hence are not dealt with by the protocol.

The premise of the arrangements in the Protocol appears to be that the UK’s regulations for goods will be less demanding than the EU’s, and that the UK will maintain customs duties (tariff rates) no higher than the EU’s for every single commodity. Practically, the former means assuming that any good acceptable in the EU (and hence RoI) will be acceptable in the UK, but not vice versa. The latter implies that no import from outside the EU and UK combined will be taxed more by the UK than the EU, so that there will be no incentive for goods to enter the UK via the EU. Whether taxes (tariffs) will need to be levied on EU-UK trade will depend on the final trade arrangements agreed, although the intention stated in the Political Declaration is that there should be none.

The asymmetries just described mean that while the UK government sees no need to impede the flow of goods from the EU to the UK, the opposite is not true. Maintaining the integrity of the European Single Market and Customs Union will require structures and processes to manage the flow from the UK to the EU, and these are the main content of the trade aspects of the protocol.

As we will discuss below, the premise is bound to be violated a little and may be violated significantly. Regulations evolve over time and, as they diverge, the UK and the EU are likely to end up in different places, depending, inter alia, on the views of the Government and the Union at the time. Quite what this implies for the structures proposed in the Protocol is unclear, but the introduction of additional impediments to trade flowing from the EU to the UK seems unavoidable. If the government were not willing to contemplate such impediments, the premise ends up imposing a considerable limit on UK policy discretion as it implies that the UK will only ever be able to relax rather than tighten any EU regulation, a position which may feel easy to live with at present but perhaps less so in future.

A second preliminary remark is also important: as we will discuss in a subsequent section, the protocol is ambiguous or unclear in at least one important respect, and much of its detail remains to be worked out by the Joint UK-EU Committee that will underpin its operation. Thus this note cannot be entirely definitive.

The note proceeds by considering customs issues, then regulatory ones and finally the possible effects of the protocol on trade flows and, implicitly, economic activity.

Customs and border formalities

The main objective of the protocol on Ireland/Northern Ireland is to ensure that no border checks of any kind are needed at the border between Northern Ireland and the Republic of Ireland. To avoid customs checks, the UK and the EU have agreed that any good imported into Northern Ireland (NI) (including from Great Britain - GB) that is ‘at risk’ of being subsequently moved into the Republic of Ireland (RoI) (or the rest of the EU) will be subject to EU tariff rates, albeit levied by the UK authorities.

The definition of ‘at risk’ will be established by a Joint Committee (JC) before the end of the transition period, but Article 5(2) of the Protocol lays down the following criteria:

- Goods subject to commercial processing in Northern Ireland are considered at risk unless the JC deems them otherwise on grounds related to the ‘nature, scale and result of the processing’ (i.e. not on the nature of the good per se)

- Other goods are subject to JC decision on criteria related to ‘the nature and value of the good, the nature of the movement and the incentive for undeclared onward movement’, including the tariff differential between UK and EU rates and the ease of transportation.

The share of Northern Ireland’s imports facing tariffs determined by the EU will depend crucially on the decisions made by the Joint Committee. However, based on the information available, previous analysis by the UKTPO estimates that around 75% of Northern Ireland’s imports (including purchases from GB) could face tariffs determined by the EU (full analysis).

Despite this, Article 4 of the protocol states that:

Northern Ireland is part of the customs territory of the United Kingdom.

There is a question, then, of whether or not Northern Ireland should de facto be considered to fall under the UK’s or EU’s customs territory, or perhaps both. This question is currently under dispute, with a legal case pending to be heard at the Scottish Court of Session (more details).

The dispute arises in light of Article 55(2) of the Taxation (Cross-border Trade) Act 2018, which states that:

For the purposes of this section “customs territory” shall have the same meaning as in the General Agreement on Tariffs and Trade 1947 as amended.

A customs territory is defined by Article XXIV(2) of the GATT as:

For the purposes of this Agreement a customs territory shall be understood to mean any territory with respect to which separate tariffs or other regulations of commerce are maintained for a substantial part of the trade of such territory with other territories.

The outcome of the legal case is at time of drafting unknown, and will likely depend on the interpretation of a ‘substantial part of trade’ in Article XXIV(2). The definition of a ‘substantial part’ is intentionally different from Article XXIV(8), which requires that free trade areas cover ‘substantially all’ trade. (Footnote 1). However, no further clarification or case law exists to shed additional light on the definition of a ‘substantial part’.

If it is ruled that the customs arrangement under the Protocol does not satisfy the definition of a ‘substantial part of trade’, there seem to be 3 possible outcomes:

- First, Northern Ireland might be deemed to fall under the EU’s customs territory.

- Second, it could be considered to operate under 2 customs territories simultaneously (the EU’s and the UK’s), although we know of no precedent for this (Footnote 2).

- Third, Northern Ireland could be declared to be its own separate customs territory, within the United Kingdom.

There are several precedents for separate customs territories falling under a common sovereignty (historically relating to relationships with colonies). However, it would cause certain complications in this case, such as having to negotiate separate trade agreements for Northern Ireland, including in the Rules of Origin they use, and writing a trade agreement between the Northern Irish and Great British customs territories that evaded all possibilities of their mutual trading arrangements having to be extended to others via the most favoured nation clause.

Irrespective of the juridical status of the Northern Ireland customs territory, in practice, there will be 2 different tariff regimes operating in Northern Ireland: the UK’s tariff regime for goods deemed not ‘at risk’, and the EU’s tariff regime on all goods deemed ‘at risk’. Having dual tariff regimes inevitably brings complications, related to the difficulty in identifying the correct tariff regime for a good, the processes needed to administer the proposed rebate scheme, and the need for customs checks at the border between GB and NI.

Customs checks required on goods sent from GB to NI

The EU tariff will apply to any goods sent from GB to NI which are deemed at risk of being subsequently transferred into RoI or the rest of the EU. In the absence of a Free Trade Agreement (FTA) between the UK and the EU, the EU’s Most Favoured Nation (MFN) tariffs would be levied on British goods sent to NI which were ‘at risk’. This would require customs checks at the GB-NI border (or an alternative location) to ensure that GB exporters had paid these tariffs before the goods entered NI.

If the UK and the EU agree an FTA, and assuming that it covered all goods, this would eliminate the need for tariffs on GB exports to NI. However, it would not fully eliminate the need for customs checks. In a UK-EU FTA, only goods originating in the UK would qualify for duty free access to the EU. The FTA would specify origin requirements which goods from GB would need to satisfy in order to be considered UK-made and receive preferential treatment. Thus, even under a FTA there would need to be at least the threat of customs checks at the GB-NI border to ensure compliance with the rules of origin.

Will border formalities be required on goods sent from NI to GB?

It is difficult to predict what level of border formalities (if any) there will be on goods shipped from NI to GB. Article 6(1) of the Protocol on Ireland/Northern Ireland states that:

Nothing in this Protocol shall prevent the United Kingdom from ensuring unfettered market access for goods moving from Northern Ireland to other parts of the United Kingdom's internal market.(…)

This has been repeatedly confirmed in statements by the government, with Mr Johnson stating that:This has been repeatedly confirmed in statements by the government, with Mr Johnson stating that:

This is a matter for the UK government and we will make sure that businesses face no extra costs and no checks for stuff being exported from NI to GB." (BBC News, 15 November 2019)

At the same time, Article 5(4) confirms that the Union Customs Code (UCC) will apply to Northern Ireland. Article 271 of the UCC requires that exit summary declarations are lodged when goods are taken out of the customs territory of the Union. Since Great Britain will no longer be part of the customs territory of the EU, this applies when a good is sent from NI to GB. Indeed, evidence to the House of Lords EU Select Committee the Brexit Secretary Stephen Barclay confirmed that such exit summary declarations would be required at the NIGB crossing.

Articles 6(1) and 5(4) thus appear, prima facie, to conflict, although ‘nothing … shall prevent’ might seem to prevail. If so, the question shifts to the interpretation of ‘unfettered’. This would appear to be a matter of law, which would ultimately, unless there is already a private understanding, need to be negotiated by the parties. Art. 169 of the Withdrawal Agreement states that in the event of a dispute, the UK and the EU should try to resolve this by “entering into consultations in the Joint Committee in good faith, with the aim of reaching a mutually agreed solution”. If no agreement is reached, an arbitration panel can be established to make a ruling on the matter (Footnote 3). This area is complex and further advice may be required.

The underlying reason why there would need to be customs checks at the GB→NI border is for the EU to ensure that no products can circumvent the EU tariff by being shipped from GB to NI, and then subsequently from NI to RoI. This would be particularly pertinent if the UK were to sign an FTA with a partner with which the EU did not have one. In theory, the same risks apply in the other direction – without any customs checks on goods sent from NI to GB, there may be a risk of exporters circumventing the UK’s tariffs by shipping goods from RoI to NI, and thence to GB. In any event, with an open border between NI and RoI, establishing the origin of goods for the purposes of either an EU or UK FTA is likely to be quite testing.

The risk of circumvention would be particularly relevant if no trade agreement is in place between the UK and the EU, in which case there would be an incentive for EU exporters to avoid the UK’s MFN tariff by shipping their products through NI into GB tariff free. However, even if an FTA is in place between the EU and the UK there may still be a risk of circumvention if the rules of origin requirements are not enforced. As noted above, the UK is working on the assumption that the UK’s MFN tariffs will always be lower than the EU’s MFN tariffs, and therefore that the latter risk is negligible. However, this cannot be guaranteed – indeed, it is likely to be violated. For example, if a country has a preferential trade agreement with the EU but not with the UK, this country could send its products to RoI duty free, and these products could then be sent through NI to GB, thereby avoiding UK’s MFN tariffs. Likewise, given that the UK and the EU will be obliged by WTO rules to set their trade defence instruments, such as anti-dumping duties, according to local conditions, it is inevitable that at some stage the UK will settle on a higher anti-dumping duty than the EU.

The UK government has discretion over whether or not it considers the risk of circumvention a price worth paying in order to avoid customs checks on goods sent from NI to GB. However, failing to implement customs checks may make the UK liable to challenge on the grounds of violating its obligations under WTO.

GATT consistency

The World Trade Organization’s principle of non-discrimination is a cornerstone of the multilateral trading system. The General Agreement on Tariffs and Trade (GATT) Article I (General Most-Favoured-Nation Treatment) requires that any advantage granted by a WTO Member to the goods of another Member must be extended unconditionally to like products of all other Members. This covers not only customs duties, but also “all rules and formalities in connection with importation and exportation” (GATT Article I).

As discussed in the preceding sections, with no checks between NI and the EU (notably RoI), and if there are no checks at the border between NI and GB, this means that products from the EU could be sent to NI, and onwards into GB, without facing any tariffs or regulatory/administrative checks, even if no FTA is in place between the UK and the EU. In contrast, products imported from non-EU countries, for example the USA or Australia, would face tariffs and regulatory checks. Thus, products from the EU would be treated more favourably than like products from countries outside the EU, which would be in violation of the Most Favoured Nation (MFN) principle.

Further, as mentioned earlier, products from countries with which the EU has an FTA, but not the UK (for example Japan or Canada), could be imported into RoI tariff free, and then sent on to GB, via NI, tariff free. This would mean, for example, that Japanese products receive more favourable treatment than products from the USA or Australia, again, probably breaching the UK’s MFN obligation.

Article XXIV of the GATT outlines some exceptions to the MFN rule. First, XXIV(3) states that the agreement does not prevent any advantages “accorded by any contracting party to adjacent countries in order to facilitate frontier traffic”. Further, according to XXIV(5), if 2 or more countries enter into a free trade agreement or customs union they are entitled to grant each other better treatment, without having to extend the same to other countries not party to the agreement.

It is unlikely that the exception for ‘frontier traffic’ would be of any help in the Irish scenario. No case law exists for this provision and although the preparatory committee advised that the definition of ‘frontier traffic’ could vary for each case, and should therefore not be too narrowly defined, an early draft of the provision limited it to 15 kilometres from the frontier (GATT Part III Article XXIV). As such, it seems unlikely that this could be interpreted to apply to the whole of Northern Ireland.

In addition, while an FTA between the UK and the EU would largely resolve the issue of differential tariff treatment, the questions of regulatory checks and rules of origin would remain, so there would still remain some checks for business to complete on NI→GB trade.

Ultimately, with an open border between NI and the EU, and without any checks carried out at the NI-GB border, if 2 countries, neither of which had an FTA with the UK but one of which had an FTA with the EU, wanted to export the same product to the UK, there would be no way for the UK to prevent the country with an EU FTA from exploiting the RoI-NI route in order to gain tariff-free access also to the UK market, while the other country would face tariffs at all entry points. In such a scenario, the UK would almost certainly be in breach of the WTO’s MFN principle. However, this would only be established, and have direct consequences for the UK, if another member instituted a dispute with the UK about it in the WTO.

Several other parts of the WTO pose potential problems for any arrangement that applies rules in different ways on different borders – as the UK would be doing under the Protocol. GATT Article X, in the words of the WTO Appellate Body, ‘establishes certain minimum standards for transparency and procedural fairness in the administration of trade regulations’. It also requires that there is ‘uniformity’ in the administration of trade-related regulation. In other words, countries should not treat some goods – or some countries – much differently than others in the administration of customs procedures. There are a dozen or so disputes focusing on this requirement. A light-touch approach applied only on one border could certainly prompt another - likewise, there is a possibility that the EU could face complaints of a similar nature (Footnote 4).

Article 10.7 of the Trade Facilitation Agreement, which recently entered into force, also obliges each WTO Member to ‘apply common customs procedures and uniform documentation requirements for release and clearance of goods throughout its territory.’

Regulatory divergence

The protocol accepts that a substantial number of EU directives and regulations will be applied in NI, in order that an open RoI-NI border does not endanger the EU Single Market that operates in RoI. If GB diverges (‘downwards’) in these dimensions, this will mean that goods that are acceptable in GB will not be permitted on the market in NI without additional assurances. For goods coming from GB – either locally produced or imported – this will be enforced as, or before, the goods leave GB ports. It will require that the goods conform to EU regulations and are certified – possibly self-certified – as such. Thus, while this process protects the EU Single Market, it will create frictions in the UK internal market, which could have an impact on trade between GB and NI, an issue to which we return below.

Any certification process will be more burdensome than the status quo, where UK adherence to the agreed Single Market regime means that any good fit to be put onto the market in the UK is deemed fit to be exported to any part of the EU. Where self-certification is sufficient, exporters will still have to take steps to ensure that they are aware of their obligations and undertake record-keeping and some investigation to assure themselves that they meet EU requirements. Where third-party certification is required, procedures are bureaucratically burdensome and involve expense, and this is especially so if it can be provided only by agencies in the EU. The alternative of UK agencies providing certification is probably easier for GB exporters, but the agencies themselves will still need to receive approval from the EU, unless the UK and the EU agree on mutual recognition of certification, whereby autonomous UK agencies will be able to certify UK exports. Such mutual recognition is difficult and slow to achieve in FTAs, however.

Once certification has been provided most manufacturing consignments are not checked, but there has to remain the possibility of paper checks and occasional physical checks to make the system credible. Consignments of foodstuffs are subject to far more surveillance and much of this takes place at the point of entry (or exit), even if this is removed from the physical border. Food inspections can require specialist staff and/or facilities. Hence regulatory divergence between GB and NI will entail paperwork and border formalities on GB→NI trade, with inevitable increases in costs and probably time-use.

Goods from a non-EU trading partner that enter NI directly rather than via GB will have to satisfy the EU regulations as they do at present, so the protocol implies no change.

It is worth re-iterating that if, at any point, regulations in the UK demanded something not required by EU regulations, processes similar to those just outlined will have to be applied to NI→GB trade, with all the attendant cost and inconvenience (a further de facto constraint on UK policy discretion). Moreover, any such differences will potentially impose costs on producers supplying the UK market – they will have to maintain some difference between their offerings to the EU and to the UK. Since the latter will be only a 6th of the size of the former, these costs will tend to be passed on to UK consumers/users. The effect might be offset if the UK regulation allows significantly lower costs, but in general this does not seem very likely. Apart from the so-called level playing field issues, the UK is not likely to deviate very far from the EU for many years because goods regulations are mostly defined by standards (which the UK seems intent of maintaining in alignment) and concern technical issues like safety and compatibility. An added complication is the fact that many areas of agriculture and the environment fall within devolved competencies. In the absence of agreed UK-wide common frameworks in these areas there is a risk that one or more of the devolved nations adopt a different approach to the rest of the UK, creating further frictions in the UK internal market (Footnote 5).

Regulation and FTAs

In terms of regulation, the market in NI will look to potential suppliers exactly like the one in RoI and the rest of the EU. Thus, to all practical purposes, running a separate regulatory regime will amount to hiving off the 2% of the UK market that is in NI to the EU (ONS Gross Domestic Product at market prices for UK). This will be reinforced to the extent that the goods face EU tariff-rates because they are ‘at risk’ of onward transfer to the Union. This will make the UK marginally less attractive as an FTA partner than if the UK were accessible complete. However, given that that it is only 2% of demand and that the regulatory differences will not affect all goods, the overall effect is likely to be small in total.

The effect may well not be negligible for NI, however. Potentially, very few of their imports from FTA partners will benefit from the agreements. Moreover, NI producers will not be able to take advantage of any relaxation in regulations that the UK government undertakes as a result of an FTA, because they will still be bound by EU regulations. NI exporters will still be able to benefit from any concessions that an FTA partner offers the UK, but they might operate under higher costs than GB firms. (It is, after all, one of the principal objections to remaining in the EU that the regulations imply inefficiencies) (Footnote 6). The net effect is likely to be that NI reaps little benefit from supposedly UK-wide FTAs.

The direct trade effects just discussed are probably not very large, but there is also a potentially more important indirect effect. It is that any FTA agreement that the UK signs that recognises regulations and certification as areas of potential integration will require the inscription of a swathe of exceptions for NI. Similarly, it may prove necessary to inscribe explicit exceptions to note that many of the partner’s exports to NI will probably face higher EU tariffs. In any negotiation asking for exceptions is potentially costly, and may stimulate the partners to seek concessions or to ask for their own exceptions. For example, if the UK seeks to except Northern Ireland from part of a deal, might not the partner seek corresponding exceptions for itself? We have been told by an insider that during the NAFTA negotiations, the USA extracted concessions from Canada in return for Quebecois exceptionalism.

Potential changes in trade patterns

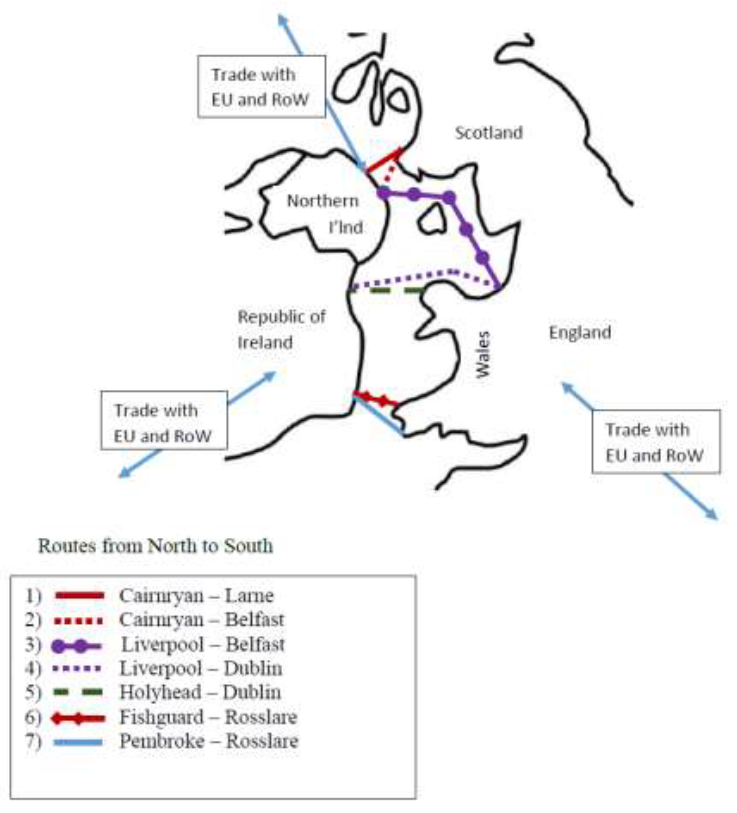

For the next several years, Brexit will inevitably reduce the amount of trade between the UK and the EU. There is room to argue about by how much, but nothing is occurring to increase trade and much is happening that might reduce it. Hence, ceteris paribus, we would expect some diminution of the trade flows crossing the Irish Sea. We do not discuss the overall effect any further, but rather focus on the way in which the Protocol on Ireland/Northern Ireland changes the incentives for trade on different routes between Great Britain and the island of Ireland (II), including those flows that occur within the United Kingdom.

Figure 1 outlines the main sea trade routes between GB and II. For UK purposes the key distinction is between routes (1)-(3), which, covering GB-NI trade, are internal to the UK and routes (4)-(7) which are between GB and RoI. For the Welsh Government, a further distinction is between (4) and (5)-(7) because the latter trio are via Wales. We proceed on the assumption that there is no realistic prospect of opening a Wales-NI route (e.g. Holyhead- Warrenpoint?).

For Northern Ireland, the protocol means that imports from GB will face customs checks, other regulatory/administrative checks and often tariffs. In contrast, NI trade with the EU (notably RoI) will remain frictionless. As a result, trade within the II will become easier relative to trade between NI and GB. It is therefore likely that GB will lose market share in Northern Ireland, both to domestic (NI) supply and to imports from the EU.

Figure 1: Sea routes between Great Britain and Ireland

While GB→NI trade seems destined to decline, it seems unlikely to do so to the same extent as GB→RoI trade. First, trade that can be proven to remain within NI will be exempt from tariffs (although not the other frictions) and there will be a clear incentive to minimise border checks and frictions between GB and NI, so that they may be less burdensome than those on GB→RoI routes. It is even possible that the differences in bureaucracy will be sufficient that some GB producers divert their exports destined for RoI through NI. There will be plenty of exporters – especially of time-sensitive products – who prefer the quicker transit times for the Wales→RoI routes, but presumably not all. Presuming that the arrangements for identifying products ‘at risk’ of being transferred to RoI are effective, diversion of this kind will economise only on border formalities, but it could be material. Further, an experimental data source suggests that a non-negligible proportion of the consignments travelling between Holyhead and Dublin are destined for or originate in NI. If border frictions are higher at the GB→RoI crossing than at the GB→NI one, there may be an incentive to re-route such consignments towards a direct GB→NI route.

If the EU and UK sign a FTA ensuring zero tariffs, the arguments of the previous paragraph continue to apply, but with less force because for goods meeting the ROOs, the tariff on entering NI and on entering RoI will be the same.

Turning now to NI→GB trade, if there are no, or only very light, checks between NI and GB, there will be an incentive for RoI exporters with products destined for GB to send these to NI, and from thence to GB. It is possible that for time-sensitive goods such as foodstuffs, which are understood to be a significant share of the Dublin↔Holyhead trade, these benefits will be outweighed by time considerations. However, any effects that are felt will be adverse for direct RoI-GB routes.

Overall, the more extensive are the trade barriers between the UK and the EU, and the less extensive are the border checks between GB and NI, the more incentive there will be to divert trade from RoI-GB to NI-GB routes. It is not possible at present to quantify these incentives or their effects, but it cannot be guaranteed that they will be negligible.

A second implication of any regulatory divide is that there will be some incentive for goods from third countries to enter NI, or the RoI, directly rather than via GB, because the latter will potentially involve 2 somewhat different sets of controls – as they enter GB and as they leave for Ireland. This will either reduce the flow of goods through Welsh ports (as well as others in GB), or require consignments to pass through GB in sealed containers under transit guarantee and with transit documents, potentially reducing commercial flexibility and increasing costs. And unless there is a special transit lane at borders, transit trade will be subject to the same delays as everything else. A similar issue arises for consignments travelling between RoI and the continental EU, although in this case it could redound to the advantage of Welsh ports.

At present, in both these cases, there is no issue about whether a consignment passing through GB is sealed or is subject to subtractions or additions as it passes through GB. After Brexit, however, an EU→RoI consignment that is not sealed will face import formalities on entry into the UK, and some further formalities on onward transmission to RoI. It seems likely, therefore, that a larger proportion of trade passing through GB will wish to pass in sealed containers from the EU to RoI, or from non-EU sources to NI or RoI without engaging with the UK authorities. Consequently, since Wales provides the shortest and quickest landbridge between RoI and the continent, it would be worth ensuring that transit trade is handled efficiently.

The need for new infrastructure to handle new border checks

Under the Withdrawal Agreement there would need to be checks at the border between Great Britain and Ireland. The extent of these checks will depend on the type of relationship that is agreed between the EU and the UK after the transition period, but no arrangement will reduce them relative to the status quo. Handling whichever checks are required, even if some things could be streamlined using technological solutions, will undoubtedly require increased border infrastructure in Welsh ports such as Holyhead, Pembroke Dock and Fishguard.

In evidence given to the Welsh External Affairs and Additional Legislation Committee, Ian Davies of Stena Line Ports stated that:

As a port operator, physically we do not have the land mass to stop and check vehicles. We just physically do not. We have some of the largest ferries in Europe coming in—Holyhead is a prime example—and we do not have the space even to empty those directly into the port. The whole port would come to a grinding halt, and our industry is based on just-in-time logistics.

Delays due to border checks will be particularly problematic for perishable food products, which are believed to make up a significant share of goods shipped from Holyhead to Dublin. Indeed, food products are among those likely to face increased checks, particularly if the UK diverges from EU’s food safety standards.

One final point is worth mentioning. Most consignments of animals, animal products and products of non-animal origin from non-EU countries must come through a Border Inspection Post (BIP). After the UK leaves the EU, animal products exported from GB to NI or ROI would therefore be required to enter through an authorised BIP. In Ireland, Dublin port is a BIP for ‘packed products of animal origin’ whereas horses can enter through Dublin airport and other live animals (horses, cattle, sheep, pigs and goats) through Shannon airport (Irish Tax and Customs). Similarly, Belfast Harbour and Belfast International Airport are designated BIPs for the importation of products of animal origin in Northern Ireland, but not for live animals (Footnote 7). This means that animal products currently exported through a port which is not a recognised BIP would need to relocate to an authorised BIP. If the capacity for handling animal imports is greater in Dublin than in Belfast, then there could be an incentive for exports of animal products to relocate towards the Holyhead-Dublin route. Further, although it is not currently envisaged that the UK will want to make extensive SPS checks on products entering from the EU. However if it ever did so, there would be returns to ensuring that Wales and its corresponding ports in RoI are well set up to manage them.

Julia Magntorn Garrett and L Alan Winters

UK Trade Policy Observatory

University of Sussex*

* We are grateful to Anna Jerzewska for comments on an earlier draft of this paper.

Footnotes

[1] ‘Substantially all’ is interpreted by the EU as covering at least 90% trade. For more see Lydgate, E., and Winters, L.A., “Deep and Not Comprehensive? What the WTO Rules Permit for a UK–EU FTA”, World Trade Review, Volume 18, Issue 3 July 2019, pp. 451-479.

[2] One interesting case is that of Bolivia, which is currently a member of the Andean Community, but which is also seeking to join MERCOSUR. If Bolivia accedes to MERCOSUR, and keeps its membership in the Andean Community, it would technically be a member of 2 different customs unions, which would strictly create inconsistencies. However, the Andean Community does not have a functioning common external tariff and is therefore operationally more similar to a free trade area than a customs union. MERCOSUR’s common external tariff (CET) is also subject to a range of national derogations and there is at least one case where a member of MERCOSUR (Uruguay) has signed a bilateral FTA with an outside country (Mexico). The imperfect CET means that intra-union border checks are still needed, and also that the members are still regarded as separate customs territories. Another example which has, in the past, been presented as a potential solution for the Irish border is the small German town of Büsingen, which operates under a part-German part-Swiss system. However, for customs purposes, it falls only under the Swiss customs territory. (Irish Times)

[3] According to Art. 174 of the WA, in matters concerning EU law, only the Court of Justice of the European Union (CJEU) has authority to make rulings. However, the issue here is not the interpretation of Union law – it is unambiguous that the Union Customs Code requires exit summary declarations. Rather the issue is whether ‘nothing [prevents] unfettered access’ predominates and what it means. Article 12.4 of the protocol confers certain EU powers on certain UK authorities and provides that the EU has jurisdiction over certain elements of the Protocol. However, these latter elements do not include Article 6, which includes the term ‘unfettered’, or Article 4, which defines Northern Ireland as part of the UK customs territory.

[4] Hard Brexit, soft Border. Some trade implications of the intra-Irish border options.

[5] Brexit food safety legislation and potential implications for UK trade: The devil in the details.

[6] This concern was raised in evidence to the House of Lords Select Committee, where the president of Ulster Farmers Union argued that if the UK lowered its standards vis-à-vis the EU this would put NI farmers at a disadvantage as they would still need to adhere to the higher (more costly) EU standards whereas other producers could undercut NI suppliers by producing to lower (cheaper) standards.

[7] The port of Larne is currently the only approved port of entry for livestock imports in to Northern Ireland but it is not an approved Border Inspection Post for animals or animal products - Border Inspection Posts (BIPS).