Wales tourism accommodation occupancy surveys: July to September 2021

The occupancy surveys provide trend information on the demand for tourist accommodation in Wales for July to September 2021.

This file may not be fully accessible.

In this page

Introduction

This update summarises the top line results of the Wales Accommodation Occupancy Survey. Results for this survey are reported for the period July to September 2021 compared with 2019 and 2020, as well as the quarterly averages for these periods. The exception to this are the hotel and guesthouse/B&B sectors where due to a methodological change in 2020 and 2021, comparisons with 2019 cannot be made. Figures are provisional and may be subject to final revision.

Main points

- Hotel room occupancy in July rose to 81%, a noticeable difference to the previous year when room occupancy was at 26% as most hotels were closed for part of the month due to COVID-19 restrictions. Both months of August and September saw high room occupancy levels, peaking in August at 86%, the highest occupancy across the year to date. Bed occupancy followed a similar pattern during this period.

- At the start of the peak summer months, in July guesthouse/B&B’s recorded room occupancy levels of 68% with August increasing to 76%, the highest across the year so far, and September seeing 71% of rooms occupied during the month. Bed occupancy followed a similar pattern during this period.

- Self-catering unit occupancy levels were 83% in July, down slightly from 85% in June, but a 7 and 13 percentage point increase on July 2019 and 2020 respectively. August fared well with levels peaking at 91%, on a par with the previous year (90%). September continued to see positive unit occupancy levels with occupancy considerably higher than 2019 (68%). Occupancy in the static caravans and holiday homes sector saw pitch occupancy levels higher in July and August when compared with the same months in 2020. September continued to show consistently high pitch occupancy across all three years from 2019 to 2021. The static caravan sector this year saw rates above 90% in all three months of this quarter.

- As with static caravan and holiday parks, pitch occupancy across the touring caravan and camping parks in July was strong at 65%, and continued the upturn with the peak summer month of August at 69% pitch occupancy. However, although pitch occupancy in September saw a downturn to 48%, this was still above levels in the same month in 2019 and 2020.

- July saw hostel bed occupancy levels rise to 39% compared with only 17% in 2020, still 30 percentage points below that seen in July 2019 (69%). A similar pattern was seen in both August and September with occupancy levels at 58% and 39% respectively, still significantly below the same months in 2019 (75% and 54%).

Change in weighting

During several months of 2020 and the first three months of 2021, a significant number of hotels, guesthouses/B&B’s were not open due to COVID-19 restrictions which limited serviced accommodation operating resulting in only a small number of hotels and guesthouse/B&B’s providing data, which impacted the weightings. Weighting of occupancy data is designed to adjust for different levels of response across regions and size bands but when the sample size is small the effect of the weighting for certain regions or size bands can be exaggerated. In the months of COVID-19 lockdown when sample sizes in some regions were in single figures, it would have had the effect of making individual establishments dominate the results. Therefore, the data in 2020 and 2021 is presented unweighted and only reflects occupancy levels of responding hotels and guesthouse/B&B’s which were open in the relevant month. Due to this, it should be noted that the hotel and guesthouse/B&B occupancy data shown in this report for 2020 and 2021 cannot be interpreted as representing the serviced accommodation market as a whole, and given the methodological differences, is not comparable to 2019 data shown within the hotel and guesthouse/B&B sections of this report.

Hotels

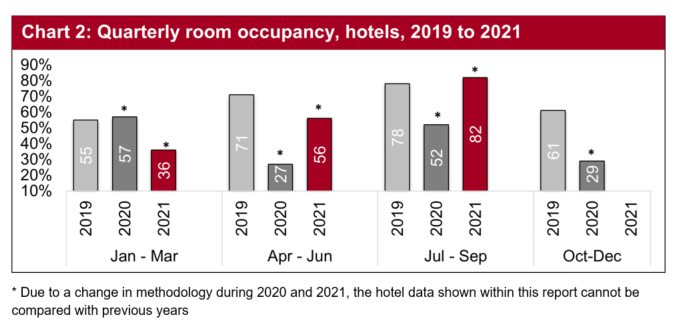

Hotel room occupancy during July rose to 81%, a noticeable difference to the previous year when room occupancy was at 26%, as most hotels were closed for part of the month due to COVID-19 restrictions, and higher than the room occupancy for July 2019 (79%). Both months of August and September saw high room occupancy levels, peaking in August at 86%, the highest occupancy across the year to date. Bed occupancy followed a similar pattern during this period.

Hotels recorded the highest room occupancy levels across the summer months of July to September of all three quarters of the year - 82%. This was 30 percentage points higher than the same period in 2020 when businesses were still affected by COVID-19 operating restrictions.

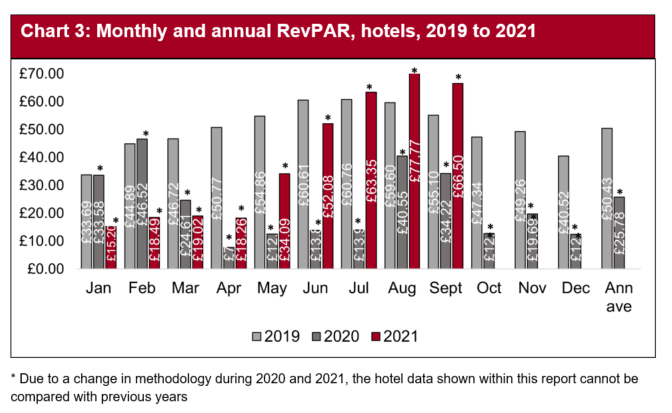

Average revenue per available room for July, August and September was £63.35, £77.77 and £66.50 respectively. August had the highest revenue per available room of the year to date, almost double that of the same month in 2020 (£40.55).

Guesthouses and, bed and breakfast

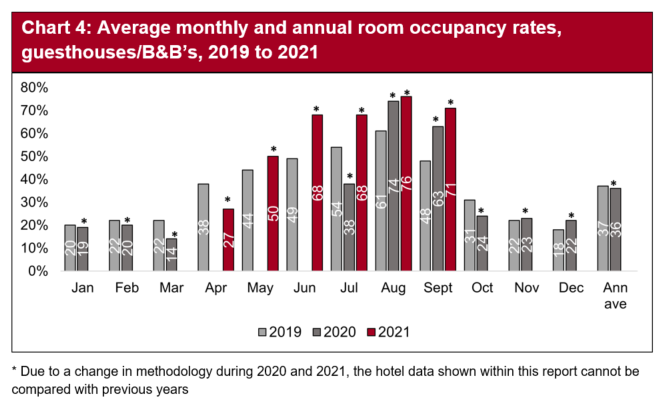

At the start of the peak summer months, in July, guesthouse/B&B’s recorded room occupancy levels of 68% increasing in August to 76%, the highest across the year so far with September seeing 71% of rooms occupied during the month. Bed occupancy followed a similar pattern during this period.

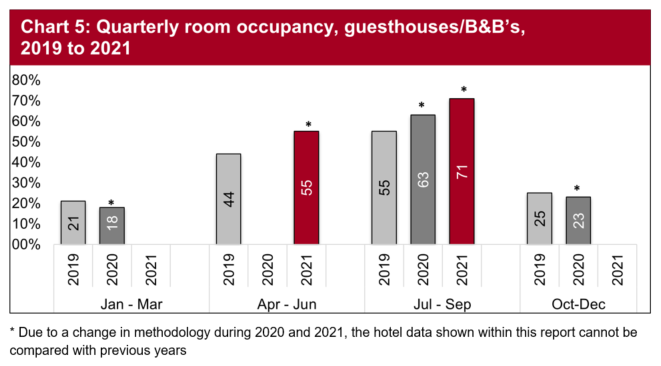

Across the guesthouse/B&B sector, room occupancy in the third quarter of the year reached 71%, 16 percentage points up on the previous quarter. However, it should be noted that the sample size was fairly small, and results should be treated with a degree of caution.

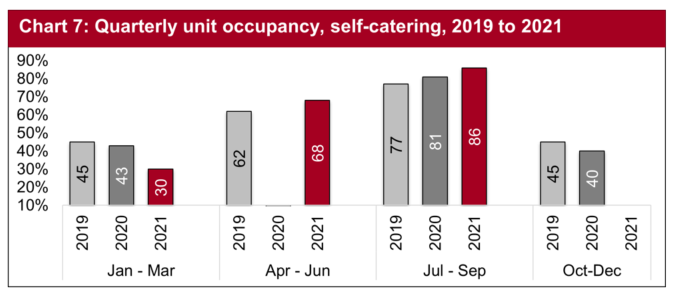

Self-catering

In the self-catering sector, July saw unit occupancy levels of 83%, slightly down on June but a 7 and 13 percentage point increase on July 2019 and 2020 respectively. August fared well with levels peaking at 91%, on a par with the previous year (90%). September continued to see positive unit occupancy levels with occupancy at 85%, considerably higher than 2019 (68%).

The quarterly unit occupancy for July to September was 86%, higher than in the third quarter of the year in both 2019 and 2020.

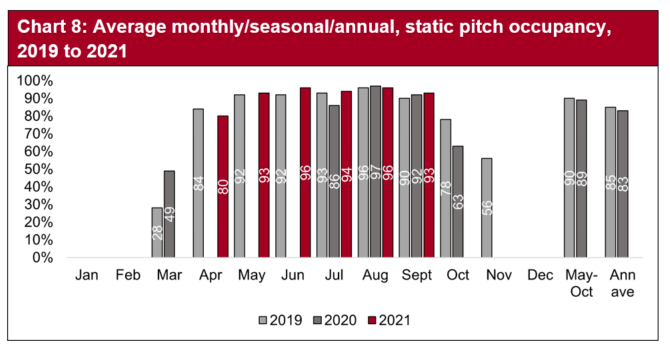

Static caravan holiday homes

Occupancy in the static caravans and holiday homes sector saw pitch occupancy levels higher in July and August when compared with the same months in 2020 and similar to those seen in 2019. September continued to show consistently high pitch occupancy across all three years from 2019 to 2021. The static caravan sector saw rates above 90% in all three months of July, August and September.

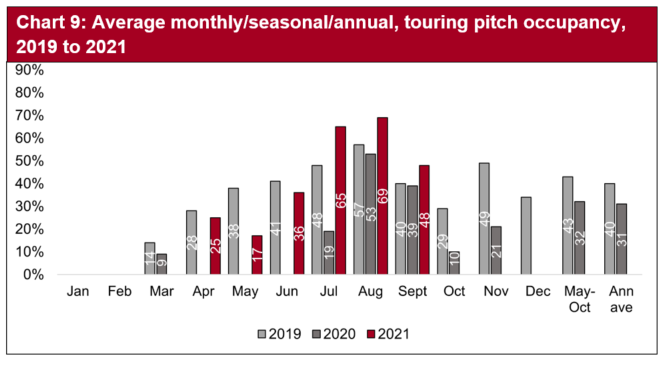

Touring caravan and camping parks

As with static caravan and holiday parks, pitch occupancy across the touring caravan and camping parks in July was strong at 65%, and continued the upturn with the peak summer month of August at 69% pitch occupancy. However, although pitch occupancy in September saw a downturn in occupancy levels to 48%, this was still above that of the same month in 2019 and 2020.

Hostels

With hostel operating restrictions due to COVID-19 impacting the number of guests permitted, lifting on 17 May, July bed occupancy levels rose to 39% compared with only 17% in 2020, however, this was still 30 percentage points below that seen in July 2019 (69%). A similar pattern was seen in both August and September with occupancy levels at 58% and 39% respectively, still significantly below the same months in 2019 (75% and 54%) but above 2020 levels.

The sector had been severely affected by the closure of hostels during the first two quarters of the year due to the COVID-19 pandemic and restrictions regarding multiple occupancy accommodation. The third quarter of the year, July to September, saw a significant rise in hostel bedspace occupancy (45%) but still not to the levels seen in the same quarter in 2019.

Context

At the start of 2021, lockdown (Alert Level 4) was still in place and continued throughout January, February, until 27 March when Wales became the first UK nation to lift travel restrictions within its borders as the stay local restrictions were ended. Self-contained tourist accommodation, such as self-catering properties and some hotels were permitted to re-open.

On 26 April, further easing of restrictions were introduced across Wales with outdoor amenities such as swimming pools were reopened, along with outdoor attractions, organised outdoor activities for up to 30 people and wedding receptions for up to 30 people were able to take place along with the reopening of outdoor hospitality.

From 17 May, remaining accommodation establishments and indoor hospitality were reopened along with pubs and restaurants who are allowed to serve drinks inside once again, while galleries and museums are also reopened.

Main timelines in 2020 and 2021

- UK National Lockdown from 23 March 2020.

- 6 July Wales lifts its “Stay Local” travel restrictions and outdoor attractions were allowed to re-open.

- Lockdown ends 11 July for accommodation businesses without shared facilities.

- Tourist accommodation with shared facilities such as camping sites were able to re-open from 25 July but any shared facilities on the premises remained closed, such as swimming pools, leisure facilities, shared shower and toilets blocks.

- Eat Out to Help Out Scheme (3 to 31 August).

- 23 October to 9 November 17-day firebreak in Wales.

- 19 December new restrictions brought in from midnight (alert level 4): non-essential retail, close contact services, gyms and leisure centres, hospitality and accommodation to close. Stay-at-home restriction. Rules were briefly relaxed over Christmas Day.

- Lockdown restrictions (alert level 4) continue in January and February 2021.

- 27 March 2021 Wales becomes the first UK nation to lift travel restrictions within its borders Self-contained tourist accommodation without shared services are permitted to re-open.

- 12 April People from Wales are allowed to travel to other parts of the UK, and UK visitors are allowed to visit Wales.

- 26 April 2021 outdoor swimming pools, outdoor attractions, organised outdoor activities for up to 30 people and wedding receptions for up to 30 people can take place along with the reopening of outdoor hospitality.

- 17 May visitor accommodation with shared services, and indoor hospitality is reopened with pubs and restaurants allowed to serve drinks, while galleries and museums are also reopened.

- 7 August with some exceptions, such as compulsory mask wearing in certain settings, most remaining COVID-19 related restrictions are lifted in Wales.

Sample size

Each of the monthly samples sizes by sector shown below are those businesses that were open and provided data for that month.

| Hotels: open |

Hotels: closed |

Guest houses and, B&B: open |

Guest houses and, B&B: closed |

Self-catering: open |

Self-catering: closed |

|

|---|---|---|---|---|---|---|

| January | 50 | 131 | 3 | 25 | 69 | 533 |

| February | 59 | 124 | 3 | 25 | 34 | 568 |

| March | 68 | 115 | 4 | 24 | 230 | 326 |

| April | 129 | 43 | 4 | 11 | 275 | 28 |

| May | 155 | 18 | 14 | 3 | 306 | 6 |

| June | 157 | 18 | 15 | 3 | 306 | 4 |

| July | 158 | 1 | 15 | 2 | 303 | 0 |

| August | 164 | 2 | 14 | 2 | 308 | 0 |

| September | 167 | 1 | 15 | 2 | 307 | 2 |

| Static caravan: open |

Static caravan: closed |

Touring caravan: open |

Touring caravan: closed |

Hostels: open |

Hostels: closed |

|

|---|---|---|---|---|---|---|

| January | 0 | 19 | 0 | 25 | 0 | 22 |

| February | 0 | 19 | 0 | 25 | 0 | 21 |

| March | 0 | 19 | 0 | 25 | 2 | 20 |

| April | 15 | 2 | 8 | 7 | 5 | 15 |

| May | 16 | 1 | 12 | 1 | 18 | 1 |

| June | 17 | 0 | 13 | 0 | 19 | 0 |

| July | 18 | 0 | 13 | 0 | 18 | 0 |

| August | 18 | 0 | 12 | 1 | 18 | 0 |

| September | 19 | 0 | 11 | 1 | 19 | 0 |

Contact details

Jen Velu

Telephone: 0300 025 0459

Email: tourismresearch@gov.wales

Social research number: 7/2022

Digital ISBN 978-1-80391-429-9

![]()