Guidance on the Land Transaction Tax higher rates for purchases of residential property.

Contents

Give us feedback on this guidance

To help us improve this guidance, give us feedback (takes 30 seconds).

LTTA/8000 Higher rates for purchases of residential property

(Schedule 5 LTTA)

The legislation in relation to the higher rates for purchases of residential property is in Schedule 5 LTTA 2017.

The higher rates of tax chargeable are set out in the regulations made by the Welsh Government and approved by the Welsh Parliament.

The rates currently in force from 22 December 2020 are set out below.

LTTA/8010 Transactions to which the higher rate apply

The higher rates apply when a taxpayer, alone or with others, buys a major interest in one or more dwellings, and the relevant conditions are met and none of the exclusions apply. Where there are 2 or more buyers who are individuals, the higher rates rules apply if they apply to any one of the buyers. Separate rules apply to acquisitions where the buyer, or one of the buyers, is not an individual.

LTTA/8020 The higher rates conditions for individuals

(paragraphs 3, 11 and 20 Schedule 5)

Higher rates apply to a transaction according to specified conditions. These conditions differ depending on whether the buyer is an individual buying a single dwelling, an individual buying 2 or more dwellings or where the buyer is not an individual (e.g. a company).

Individuals buying a single dwelling

Where the buyer, or each of the buyers is an individual buying a single dwelling the conditions are:

- the buyer, or buyers, are all individuals

- the main subject matter of the transaction is a major interest in a dwelling

- the chargeable consideration given for that major interest is £40,000 or more

- the buyer, or one of the buyers, or their spouse or civil partner that they live with, has a major interest in another dwelling at the end of the day of the effective date of the transaction (including a major interest which has been purchased for a minor child), and

- the interest in that other dwelling has a market value, on the effective date of the acquisition of the major interest in the new dwelling, of £40,000 or more

- the interest acquired is not subject to a lease for an unexpired term of more than 21 years to someone who is not connected with the buyer

Individuals buying 2 or more dwellings

Where the buyer, or each of the buyers is an individual buying 2 or more dwellings the conditions are:

- the buyer, or buyers, are all individuals

- the main subject matter of the transaction consists of major interests in 2 or more dwellings and at least 2 of the purchased dwellings meet the conditions above

- the chargeable consideration given on a just and reasonable basis for that major interest in the purchased dwelling is £40,000 or more

LTTA/8021 The higher rates conditions for non-individuals (conditions for companies)

Where:

- the buyer, or one of the buyers, is not an individual, and

- the main subject matter of the transaction is a major interest in a dwelling, or major interests in 2 or more dwellings, and

- the chargeable consideration given for that major interest is £40,000 or more (the deemed market value rule may apply - see LTTA/2460 for further details)

the transaction will be subject to higher rates.

LTTA/8030 Major interest

Schedule 5 to LTTA provides that a transaction is a higher rates transaction where the main subject-matter of the transaction consists of a major interest in a dwelling.

In turn, a major interest is defined (at section 68) as being an estate in fee simple absolute (freehold) or a term of years absolute (leasehold) subsisting at law or in equity (although leases granted for a term of less than 7 years are exempted).

Where land is held in Wales, the legal interest in the land is separated from the beneficial interest, which is also known as the economic benefit of the property.

In order to be a higher rates residential property transaction sub-paragraphs 3(2), 11(2) and 20(1) of Schedule 5 provide that the main subject-matter of that transaction must consist of a major interest. Not every transaction involving the transfer of a beneficial interest in residential property would be a transaction, the main subject-matter of which consists of a major interest (except as provided for in the Act for the purposes of the Act).

The vast majority of transactions involving residential dwellings are likely to involve the transfer of both the legal and beneficial interests. However, the legal ownership is separate from the beneficial ownership and the legal owner or owners will not necessarily be the same as the beneficial owner or owners.

The legal owner holds the beneficial interest in the property on trust for the beneficial owner. The beneficial owner will have a right to the income from the property or a share in it, and a right to the proceeds of sale of the property or part of the proceeds. The value therefore lies in the beneficial interest.

Where a property is purchased in joint names there is a trust of land. In such cases the buyers hold the legal estate as joint tenants and hold the beneficial interest in the property as either joint tenants or tenants in common.

Joint tenants are entitled to an equal share of the property. A key feature of a joint tenancy is the right of survivorship which means that upon the death of one co-owner, that co-owner's interest in the property will pass to the surviving co-owner by law.

Tenants in common hold the property in either equal or unequal shares which are known as undivided shares. An undivided share may be transferred to a third party. A transaction effecting the transfer of an undivided share may also involve a change in ownership of the legal estate, or it could relate to the beneficial interest alone.

Due to the possibility of beneficial interests being transferred separately from the legal interest, the policy intention is that transactions involving such transfers should be caught by the higher rates provisions, if the other conditions apply.

Jointly owned property

(Paragraphs 5(3)-(6) and 15(3)-(6))

Where a transaction meets the various conditions set out in Schedule 5, it is a higher rates transaction. One of these conditions is that a buyer who is an individual already has a major interest in another dwelling. Paragraphs 5 and 15 of Schedule 5 refer to the buyer having a major interest in another dwelling, and that interest having a market value of £40,000 or more. The buyer may hold that other dwelling jointly with another person.

This provides that when assessing whether this condition is met, the market value of the interest in the other dwelling is based on the buyer’s individual beneficial interest (as a proportion of the total value of the dwelling) rather than being based on the whole of the major interest.

Where the buyer is married or in a civil partnership, their interest will be combined with that of their spouse or civil partner to assess whether the £40,000 threshold has been met unless they are no longer living together (as defined by paragraph 25(3) of Schedule 5 LTTA) at the effective date of the transaction concerned.

Deeming provisions

(paragraph 29)

The deeming provisions in paragraphs 27 and 28 of Schedule 5 to LTTA apply in respect of certain settlements which entitle the beneficiary to occupy the dwelling for life or to income earned in respect of the dwelling, and also in respect of bare trusts involving leaseholds.

The effect of these deeming provisions is that it is the beneficiary rather than the trustee who is treated as the buyer (or as holding, or disposing of, an interest in a dwelling). The deeming provisions mean that it is necessary to look through the trust (be that a bare trust or the specific type of settlement trust specified in the paragraph above) to the beneficiary to determine whether the higher rates apply. This ensures that the right person is liable for the tax (i.e. the person who has the economic benefit of the property).

The aim of these rules is to put it beyond doubt that residential transactions involving the types of beneficial interest mentioned above will be caught by the higher rates provisions, even where there is no change in the owners of the legal estate.

These rules treat the subject matter of that type of transaction as one consisting of a major interest where, immediately prior to the transaction, the seller was deemed to own a major interest by virtue of the deeming provisions, and immediately after the transaction, the buyer is likewise deemed to own the major interest.

This will mean, for example, that where a person acquires only an undivided share in a dwelling (under a tenants in common arrangement), but the legal owners and other tenants in common retain their interest in the dwelling, then the acquisition will still be treated as an acquisition of a major interest. It will be subject to the higher rates (provided the other conditions are met).

Interest acquired is a lease originally granted for less than 7 years

(paragraph 37 Schedule 5)

A leasehold estate that did not exceed 7 years on the date it was granted is not a major interest, for the purposes of the application of the higher rates of LTT.

Major interest acquired is subject to a lease

(paragraphs 3, 13 and 20 Schedule 5)

A major interest in a dwelling will not be liable for the higher rates where the interest acquired is subject to a lease that has an unexpired term of more than 21 years, and is not held by a person connected to the buyer of the reversionary interest. The facts in relation to the lease are to be considered at the end of the day of the effective date of the acquisition of the reversionary interest.

LTTA/8040 How to establish the value of a beneficial interest in another dwelling

(paragraphs 5 and 15 Schedule 5)

The rules for establishing if a beneficial interest in another dwelling is worth £40,000 or more, differ depending upon whether the beneficial interest in the dwelling is owned as joint tenants, or as tenants in common.

A married couple, or those in a civil partnership, have their interests, whether as joint tenants or tenants in common, combined to establish the value of the beneficial interest in the other dwelling unless they are not living together at the effective date of the transaction being considered for higher rates liability.

For joint tenants, the market value of the currently owned dwelling, at the date of the acquisition of the new dwelling, is divided by the number of joint tenants.

Tenants in common

For tenants in common the market value of the currently owned dwelling, at the date of the acquisition of the new dwelling, is multiplied by the percentage of the interest to which the buyer is entitled.

LTTA/8050 Definition of dwelling for higher rates purposes

(paragraphs 35 and 36 Schedule 5)

A dwelling for the purposes of LTTA is residential property comprising a single dwelling. A dwelling includes dwellings both in Wales and elsewhere in the world. Where the dwelling is not in England and Wales then a number of land law concepts that exist in the law of England and Wales are taken to be the equivalent in those other countries.

Similarly, the rules relating to dwellings owned by or on behalf of a minor child outside Wales, apply in the same way as they do in Wales, including in relation to the equivalent to court appointed deputies in those countries.

A dwelling for the purposes of the higher rates is a building or part of a building that is:

- used or suitable for use as a dwelling, or

- in the process of being constructed or adapted for use as a dwelling (which will include dwellings bought off plan)

Suitable for use as a dwelling is a question of fact, and consideration as to whether the residents can live independently of the residents elsewhere in the building, separate and private access to the areas of occupation etc. will be important in considering this matter. In a house of multiple occupation, the absence of a private kitchen or private bathroom will be indicative that the house as a whole is a dwelling rather than the individual rooms within that house each representing a separate dwelling.

A dwelling for the purposes of the higher rates will include holiday homes and properties let as furnished holiday lettings (including those that have restricted occupation which prevent the dwelling from being occupied all year round, and properties such as holiday park lodges).

The garden or grounds and any buildings on the garden or grounds are part of the dwelling, to the extent they are considered to be residential property for the purposes of LTTA, and the consideration given for these will also be liable to the higher rates. However, where the buildings in the garden or grounds (or a separate flat, for example a basement flat in a house) are themselves also dwellings, the buyer will be acquiring more than one dwelling as a result of their purchase and the higher rates of LTT will be payable.

Where the additional dwellings meet the conditions of the subsidiary dwellings rules then the higher rates will not apply.

Where a taxpayer acquires residential land that does not include a dwelling (for example a part of a garden) then the higher rates will not apply as the transaction does not include the purchase of a dwelling.

The main subject-matter of a transaction will also be an interest in a dwelling (such as off plan purchases) if:

- there is substantial performance of a contract

- the main subject-matter includes an interest in a building or part of a building that is being constructed or adapted under the contract for use as a dwelling, and

- construction or adaptation has not begun by the time the contract is substantially performed

If non-residential land is owned on which the taxpayer is seeking, or has obtained, planning permission to convert to residential, that major interest in the land is not treated as an interest in a dwelling until construction or adaptation actually commences. The seeking or obtaining of planning permission falls short of the process of construction or adaptation for use as a dwelling. However, in the event that such a property was sold once construction or adaptation has commenced, if the other conditions for LTT higher rates to apply to the transaction are present, the acquisition by the buyer would be liable to the LTT higher rates.

A dwelling for the higher rates of LTT does not include interests held in or acquisitions of caravans, houseboats and mobile homes.

LTT in its definition of a residential property, defines certain buildings as being residential (for example residential accommodation for school children) and certain buildings as not being used as a dwelling (for example a prison). For the purposes of the LTT higher rates rules, none of the buildings listed are subject to the higher rates.

LTTA/8060 Exclusions to the higher rates

The higher rates of LTT do not relate to:

- transactions where the consideration given for the acquisition of the interest is less than £40,000

- non-residential or mixed use transactions

- subsidiary dwellings when specific conditions are met

- replacement of a main residence when specific conditions are met

- Interests acquired in the same main residence where the conditions are met

- retaining interests in former matrimonial home following divorce or dissolution of civil partnership

- purchase by court appointed deputy for minor child

- transactions where, in certain circumstances, the interest acquired is subject to a lease with an unexpired term of more than 21 years to someone other than a connected person

Attempts to artificially circumvent the application of the higher rates of LTT, may be challenged by the WRA through the application of the General Anti-avoidance Rule (GAAR).

LTTA/8070 Non-residential and mixed transactions

Where a taxpayer acquires a major interest in, 6 or more dwellings in a single transaction, the taxpayer has the option to treat the transaction as a non-residential transaction. If the taxpayer opts for this treatment then the non-residential rates of LTT are used to calculate the taxpayer’s liability. Alternatively they could treat the transaction as residential and, if a claim is made, apply the rules for multiple dwellings relief. If this option is followed then the LTT higher rates are used to calculate the liability.

Where a taxpayer enters into a mixed-use transaction, for example a farm or a shop with a flat above, the non-residential rates of tax will apply to the transaction.

It is important to note that whilst the acquisition of the property may be taxed at non-residential rates, that tax treatment does not make the dwellings non-residential property when the interests in dwellings a taxpayer holds must be considered for future transactions.

LTTA/8080 Subsidiary dwelling exception

(paragraph 14 Schedule 5)

Where:

- an individual, or group of individuals, buys more than 1 dwelling to replace their main residence, or;

- an individual, or group of individuals, buys more than 1 dwelling and they do not own any other interests in dwellings

higher rates may not apply to the transaction where:

- the additional dwelling or dwellings are within the same building or in the grounds of the other dwelling (the “main dwelling”), and

- the amount of consideration given, based on a just and reasonable apportionment for the main dwelling is more than or equal to 2 thirds of the total consideration given

These additional dwellings are called subsidiary dwellings. And where the conditions are met, the transactions benefit from the subsidiary dwelling exception and should be taxed at the main residential rates.

In most cases, the valuation of the main dwelling should include all the garden and grounds, and any outbuildings (not including the subsidiary dwelling(s)).

There may be cases where as a matter of fact part of the garden or grounds clearly exist solely for the benefit of the subsidiary dwelling. In these cases, the taxpayer should exclude that part of land from the valuation of the main dwelling.

This subsidiary dwelling exception can also apply where there is more than 1 additional dwelling.

Where:

- the transaction includes 2 or more additional dwellings that are within the same building or in the grounds of the main dwelling, and;

- the consideration on a just and reasonable apportionment for the main dwelling is more than or equal to 2 thirds of the total consideration given

The subsidiary dwelling exception will apply and the transactions should be taxed at the main residential rates.

The subsidiary dwelling must be a dwelling in its own right on the effective date of the transaction. This means that it should be able to support somebody living independently of the main dwelling. The dwelling must be private and secure.

To decide whether a property contains one or more dwellings, a number of factors should be taken into account. The following factors are indicative of whether something is a dwelling or suitable for use as a dwelling in its own right. There is no single factor that outweighs the others; they should all be taken into account. The factors should be applied to the property as it is/was on the effective date of the transaction.

- A toilet and washing facilities.

Each dwelling should contain a toilet, sink (other than the kitchen sink) and bath or shower.

- Accommodation for both ‘living’ and sleeping.

In each dwelling, there should be space for a bed, somewhere to sit and somewhere to eat.

- The facility to store, prepare and cook food, as well as ‘wash up’

Each dwelling should contain a kitchen that would normally include an oven and/or hob, hot and cold running water, a space to prepare food (for example a counter top) and a space to store food.

- Independent access to both dwellings.

If the subsidiary dwelling is in the same building as the main dwelling, a door directly to the outside is not necessarily required; the property may be entered via a communal hallway/landing area. If, however, access is through the living area of the main dwelling, then it is unlikely to be classed as a subsidiary dwelling.

- If it is possible to access the subsidiary dwelling from the main dwelling (and vice-versa) there should be a lockable door in place.

- The occupant should be able to have some control over the supply of utility services.

Where the 2 parts of the property have independent controls over utilities (including electrical consumer unit, stopcock, gas/oil isolation valve, thermostat), this suggests that each part may be a separate dwelling in its own right. However, the absence of these facilities does not necessarily indicate a single dwelling.

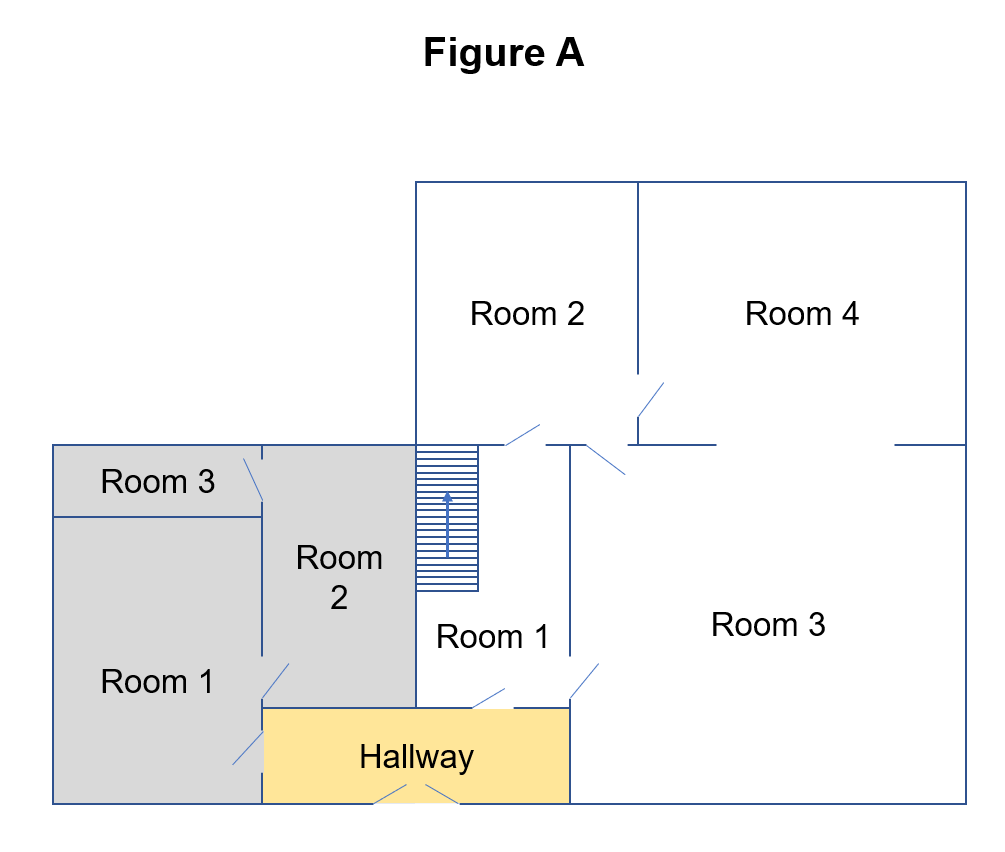

These tests should be applied to the entire property, not just to the subsidiary dwelling. For example, where works have been undertaken on a single house to create an annex, but the only kitchen in the building is within the annex, this is unlikely to be viewed as a main dwelling and a subsidiary dwelling, but rather a single dwelling.

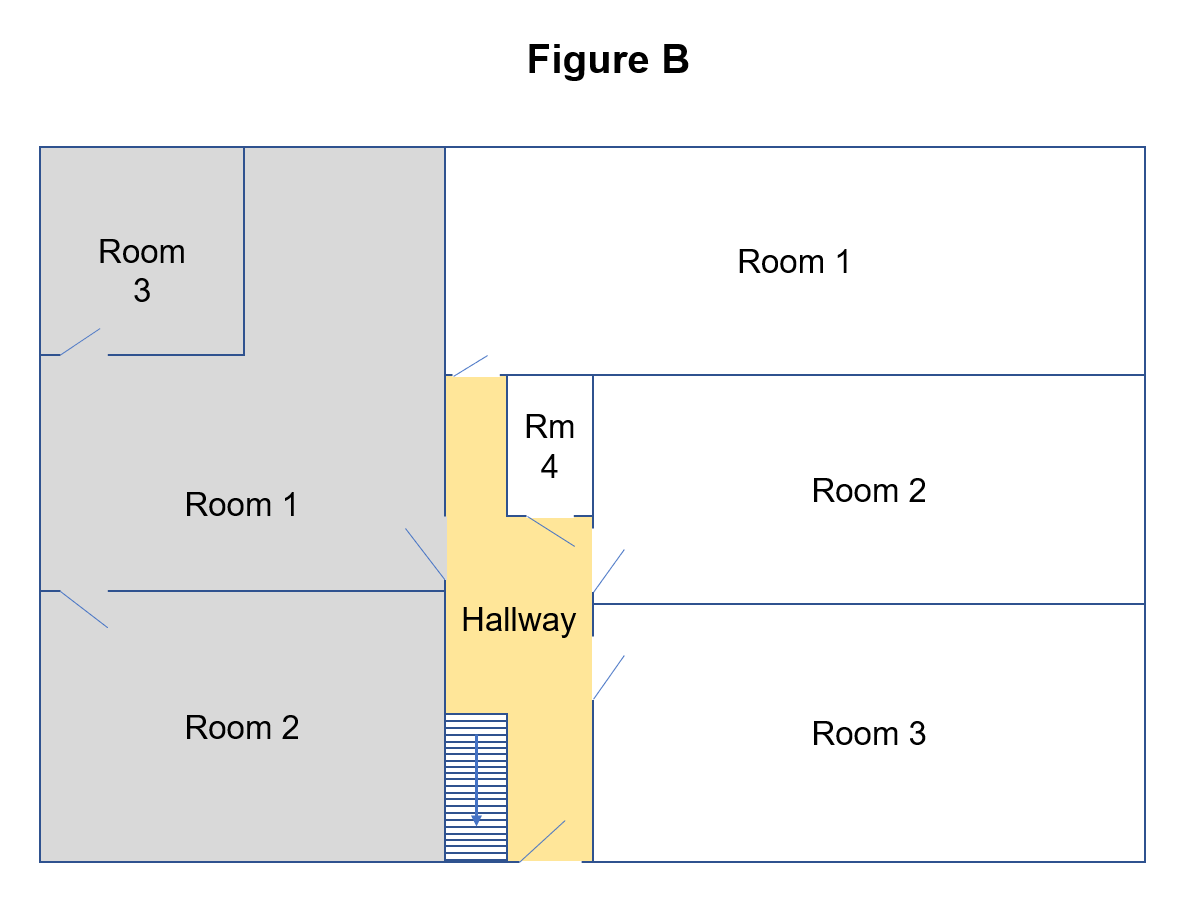

The same will be true where access to the annex is via a communal hallway which is also used by the occupants of the main dwelling to move from one room to another in the main dwelling. The property in Figure A (below) has a communal entrance from which 2 separate parts of the property can be accessed. This is more likely to mean the property comprises of 2 dwellings.

However, in Figure B (below) there is a hallway from which a number of rooms can be accessed and it is necessary to use the hallway to move between the living quarters of part of the property. This is less likely to mean that the property is split into 2 separate dwellings.

Removing fixtures alone is unlikely to make the property unsuitable for use as a dwelling. In most circumstances, the pipework and circuitry will remain, meaning that the items could easily be re-installed.

The presence of planning permission for an annexe or similar is indicative of there being more than one dwelling on the property. In addition, disaggregation for Council Tax Purposes is indicative of the property comprising of more than one dwelling.

LTTA/8090 Replacement of main residence

(paragraphs 8 and 17 Schedule 5)

A taxpayer who sells their main residence and replaces it with a new only or main residence (‘main residence’) either within 3 years before the sale of the former main residence, or within 3 years after the main residence is sold, may pay the main rates on the transaction rather than the higher rates.

To qualify for this exception, the sold property must have been the taxpayer’s only or main residence at any time in the period of 3 years before the effective date of the transaction (the purchase of the replacement main residence).

In respect of transactions where the main residence is disposed of within the period of 3 years after the replacement is acquired, the taxpayer must apply the higher rates rules to the transaction on the effective date of the relevant transaction and pay the higher rates of LTT. In the event that the relevant conditions for the replacement of main residence are met, the taxpayer may claim a repayment where necessary.

A longer period for the disposal or replacement transaction may apply. For further information on this longer period see LTTA/8121 Fire Safety Defects and LTTA/8122 Relevant Restrictions.

The rules relating to the replacement of a main residence apply only to those transactions made by an individual or individuals and not to those made by companies or other non-natural persons, or by individuals and companies or other non-natural persons jointly.

LTTA/8091 Higher rates and linked transactions

This section of guidance describes how the higher rate provisions interact with linked transactions.

Replacement of main residence and linked transactions

The replacement of a main residence exception rules apply in the scenario where:

- a taxpayer has purchased 2 or more dwellings as part of a number of linked transactions (see LTTA/2040)

- one of those dwellings replaces the taxpayers’ current main residence, and

- the dwelling which is to replace the taxpayers’ current main residence was purchased in a separate transaction from the other dwellings

Where one of the linked transactions involves the purchase of a replacement main residence and meets the criteria set out in LTTA/8090, the taxpayer is able to apply the exception to that transaction. This means that the main residential rates of tax apply to that transaction. The higher rates apply to the remaining dwelling transaction(s) in the usual way.

As the transactions are linked and one of the transactions is at main rates, and the other(s) at higher rates, to calculate the tax the taxpayer should follow a computation method which will result in an apportionment of the total consideration for all of the transactions between main rates and higher rates. The computation method can be found below.

The calculation only applies where the replacement main residence is purchased in a separate linked transaction to the other dwellings being purchased. Where the replacement main residence is purchased in the same transaction as 1 or more other dwellings, the conditions at LTTA/8020 for buying 2 or more dwellings apply.

Purchasing 2 or more dwellings where the taxpayer doesn’t have a pre-existing main residence

Where a taxpayer, who has no pre-existing interest in another dwelling and where the replacement of main residence exception does not apply, is purchasing:

- 2 or more dwellings as part of a number of linked transactions, and

- the transactions have the same effective date

the buyer will have a major interest in another dwelling at the end of the day of the effective date of each transaction, so all of the transactions will be subject to higher rates if the other conditions in LTTA/8020 are met.

Where the linked transactions are structured so that they take place on different days main residential rates will apply to the first transaction, and the higher residential rates will apply to the later additional dwelling transaction(s).

As the transactions are linked and one of the transactions is at main rates and the other(s) at higher rates, to calculate the tax the taxpayer should follow a computation method which will result in an apportionment of the total consideration for all of the transactions between main rates and higher rates. To calculate the total tax due the taxpayer should follow the computation method detailed below.

Computation method

Where a taxpayer is buying 2 or more properties as part of a number of separate linked transactions, and one of the transactions is to be taxed at the main residential rates, and the other transaction(s) at the higher residential rates then the following computation method should be followed.

- Step 1 Calculate the tax for the entire consideration (for all transactions) at the main rates.

- Step 2 Calculate the tax for the entire consideration (for all transactions) at higher rates.

- Step 3 Calculate consideration for main rate transaction as percentage of total consideration.

- Step 4 Calculate consideration for higher rate transaction(s) as percentage of total consideration.

- Step 5 Multiply the total main rates tax (calculated at step 1) by the percentage of the consideration which is to be charged at main rates (calculated at step 3).

- Step 6 Multiply the total higher rates tax (calculated at step 2) by the percentage of the consideration which is to be charged at higher rates (calculated at step 4).

- Step 7 The total of step 5 and step 6 is the tax due.

LTTA/8100 An ‘only or main residence’

It’s a question of fact as to what’s someone’s only or main residence. Not dependent upon ownership of the place of residence by the individual living in the property.

Most individuals have only one place of residence. That dwelling being their only or main residence.

For example:

- a person who owns a flat and lives there permanently

- a person who rents a flat, and it’s where they live permanently

If an individual rents a dwelling that’s their only or main residence and also owns a dwelling, they let out, even though they own one dwelling and rent the other, the dwelling they own will not be their only or main residence.

Where the individual owns more than one dwelling

Full facts need to be considered to establish where that individual’s main residence is.

Example

They live in Cardiff during the week with family and spend many weekends and several weeks during the year in Criccieth in a holiday home they own. On these facts alone, the main residence would be their Cardiff home.

There’s no opportunity in LTT to nominate one of the residences as a main residence.

But the main residence may well not be the residence where the individual spends most of their time. While usually, as above, it will be.

Nourse J noted this in Frost v Feltham (Frost v Feltham (1981) 1 W.L.R. 452):

If someone lives in two houses the question, which does he use as the principal or more important one, cannot be determined solely by reference to the way in which he divides his time between the two.

What to consider when examining what’s a person’s only or main residence

- Is the individual married, in a civil partnership, or co-habiting? If so, where does the spouse, civil partner or cohabitee live?

- Does the individual have children? If so, where do they live? Where do they go to school?

- At what residence is the individual registered to vote?

- Where is the individual’s place of work?

- How is each residence furnished?

- Which address is used for correspondence?

- Where is the individual registered with the doctor and dentist?

- Where is the individual’s car registered and insured?

- Which is the main residence for council tax?

These are not exhaustive, and no single point is determinative.

Dwellings owned or disposed of

The question will be one of objective fact. Was the old dwelling at the relevant time the individual’s only or main residence?

When considering an acquired dwelling, we look at whether it is the individual's intention that this will be their only or main residence.

Facts related to that purchase may be relevant in either:

- supporting the taxpayer’s stated intention at the point of purchase, or

- indicating a different intention

Examples:

- if the taxpayer obtains the new dwelling with a mortgage that was a buy-to-let product, this would indicate the taxpayer’s intention

- if the property was placed with a letting agent shortly after purchase, or had a sitting tenant with protected rights. It may indicate an intention not to use the property as an only or main residence

Or if the property is near family and the taxpayer intends to move closer to them to provide care. But then that support is no longer needed, perhaps due to death or that relative moving. The evidence supports that intent, even if the taxpayer does not move to that dwelling.

LTTA/8110 Sale of former main residence before buying new main residence

Please refer to LTTA/8090 when reading this guidance.

Where a taxpayer has sold their former main residence before they buy their new main residence then, where the conditions are met, the taxpayer will pay the main rates and not the higher rates of LTT, irrespective of how many other properties they may own.

The conditions are:

- on the effective date of the acquisition, the dwelling is intended to be the taxpayer’s only or main residence (‘main residence’)

- that during the 3 years ending on the effective date of the acquisition of the new main residence, the buyer or their spouse or civil partner at the time disposed of a major interest in a former main residence

- that they held no major interest in that former main residence, including any interest in the garden or grounds, following the disposal (unless a taxpayer’s spouse or civil partner retains a major interest in that property and they are no longer living with the taxpayer), and

- that no other dwelling that was intended to be a new main residence was acquired during the period between the sale of the former main residence and the acquisition of the new main residence

LTTA/8120 Sale of former main residence after buying new main residence

Please refer to LTTA/8090 when reading this guidance.

Where a taxpayer has bought their new only or main residence (‘main residence’) before they sell their main residence, or the dwelling deemed to be their old main residence, where the conditions are met, the acquisition may become a replacement of a main residence. The taxpayer will have paid the higher rates of LTT when buying the new main residence as they held, or were deemed to hold, an interest in another dwelling (the old main residence) on the effective date of the transaction in which they acquired the new main residence.

If the conditions are met, the taxpayer will be able to either amend the return under section 41 TCMA 2016 (if within the time limits permitted – 12 months from the filing date) or make a claim for repayment under section 63 TCMA 2016. The deadline for making such a claim is 4 years from the day after the filing date for the return to which the claim relates. The repayment will be the difference between the amount of LTT paid and the amount of LTT that would have been payable, had main rates applied to the transaction and not the higher rates.

The conditions are:

- on the effective date of the acquisition, the dwelling is intended to be the taxpayer’s only or main residence (‘main residence’)

- during the 3 years beginning on the day after the effective date of the acquisition of the new main residence, the buyer or their spouse, or former spouse, or civil partner or former civil partner at the time, disposes of a major interest in the buyer’s former main residence

- the property disposed of was the buyer’s former main residence at any time during the 3 years prior to the effective date of the acquisition

- that they hold no interest in that former main residence following the disposal (unless a taxpayer’s spouse or civil partner retains a major interest in that property and they are no longer living with the taxpayer)

LTTA/8121 Fire Safety Defects

A longer period than the normal 3 years (the normal permitted period) may be allowed for the disposal of the former main residence after the purchase of the new main residence if the former main residence has a fire safety defect and conditions are met. This longer period is the extended permitted period.

A fire safety defect in the sold dwelling must have at least:

- substantially reduced the number of people interested in purchasing the sold dwelling than would be the case if the property did not have the defect, or

- substantially reduced the market value of the sold dwelling than would be the case without the defect.

Each of the following conditions must be met:

- when the sold dwelling was first acquired by the buyer, or their spouse or civil partner (including former spouses or civil partners), the sold dwelling had a fire safety defect that the buyer could not have reasonably known about

- a relevant person had a duty to remedy the fire safety defect

- and either:

- the fire safety defect was not remedied on the effective date of the disposal transaction, or

- where the defect has been remedied, the disposal transaction was entered into as soon as reasonably practicable after the defect was remedied.

Who a relevant person is will depend upon the type of interest that the major interest is. For each of the below major interests, the people listed below are to be considered a relevant person.

| Leasehold Interest | Freehold Interest in Commonhold Land | Freehold Interest |

|---|---|---|

| Landlord of the person who had the major interest | Commonhold association for the sold dwelling | Developer of the sold dwelling |

| Developer of the sold dwelling | Developer of the sold dwelling |

A developer does not include a developer who is also the person who had the major interest. This means that a developer who disposes of a major interest in a dwelling affected by a fire safety defect that the developer was responsible for construction or adaptation of will not meet the conditions for a longer period unless another relevant person had a duty to remedy the defect.

Where the extended permitted period applies as the conditions in relation to fire safety defects are met, the time limit in section 78 of the Tax Collection and Management (Wales) Act 2016 for making a claim under section 63 of the same Act is replaced with two new time limits. One of these time limits will apply depending upon the timing of the disposal transaction.

When the effective date of the disposal transaction is after the regulations come into force, the new time limit will be 12 months beginning with the effective date of the disposal transaction.

When the effective date of the disposal transaction is before the regulations come into force but on or after 1 April 2021, the new time limit will be 12 months beginning with the date the regulations come into force.

If the extended permitted period applies, a claim under section 63 of the Tax Collection and Management (Wales) Act 2016 for relief for overpaid tax must be made within the applicable new time limit.

A claim that makes use of the extended permitted period must include an explanation of how the conditions for the application of that period are met. All other conditions that must be met under paragraph 8 continue to apply and must be satisfied for the replacement of main residence exception to apply.

LTTA/8122 Relevant Restrictions

A longer period than the normal 3 years (the normal permitted period) may be allowed for the disposal of the former main residence or the acquisition of the new main residence if a relevant restriction had a substantial adverse effect on the ability of the buyer to dispose of or acquire a major interest. This longer period is the extended permitted period.

A relevant restriction is a restriction or prohibition of any activity by legislation, or by a public authority using powers given to it by legislation, for the purpose of preventing, controlling or mitigating the effects of an emergency. Relevant restrictions do not include those prohibitions or restrictions that ceased to have effect before 12 July 2024.

Public authorities are persons carrying out a function of a public nature.

Emergency has the meaning given in section 19 of the Civil Contingencies Act 2004. An emergency is not restricted to only events or situations in relation to which powers are exercised under the Civil Contingencies Act 2004.

Relevant restrictions are prohibitions or restrictions of any activity by the law, or by a public authority using power given to it under the law, of that country or territory where the restrictions have effect for the purpose of preventing, controlling or mitigating the effects of an emergency.

For dwellings situated outside of the United Kingdom, references to the United Kingdom in section 19(1) of the Civil Contingencies Act 2004 are to be read as references to the country or territory where the dwelling is situated.

In the case that the new main residence is acquired after the disposal of the former main residence (also known as “Sale Before Purchase”) the following conditions must be met for the extended permitted period to apply:

- a relevant restriction came into force during the period of 3 years beginning with the effective date of the transaction in which the former main residence was disposed of (“the relevant period”)

- this relevant restriction had a substantial adverse effect on the buyer’s ability to acquire a dwelling as a replacement main residence before the end of the relevant period

- and the transaction to purchase the new main residence is entered into:

- on or after the 12 July 2024

- and as soon as reasonably practicable.

Where the above conditions are met, the buyer may self assess the main residential rates as a result of the main residence exception. The buyer must include a statement in the return explaining how the above conditions are met. All other conditions that must be met under paragraph 8 continue to apply and must be satisfied for the replacement of main residence exception to apply.

In the case that the new main residence is acquired before the disposal of the former main residence (also known as “Purchase Before Sale”) the following conditions must be met for the extended permitted period to apply:

- a relevant restriction came into force during the period of 3 years beginning with the day after the effective date of the transaction in which the new main residence was acquired (“the relevant period”)

- the relevant restriction had a substantial adverse effect on the ability of the buyer, or their spouse or civil partner (including former spouses or civil partners), to dispose of the former main residence dwelling before the end of the relevant period

- and the transaction to dispose of the former main residence is entered into:

- on or after the 12 July 2024

- and as soon as reasonably practicable.

Where the extended permitted period applies in the Purchase Before Sale scenario, the time limit in section 78 of the Tax Collection and Management (Wales) Act 2016 for making a claim under section 63 of the same Act is replaced with a new time limit.

The new time limit will be 12 months beginning with the effective date of the disposal transaction.

If the extended permitted period applies, a claim under section 63 of the Tax Collection and Management (Wales) Act 2016 for relief for overpaid tax must be made within the new time limit.

A claim that makes use of the extended permitted period must include an explanation of how the conditions for the application of that period are met. All other conditions that must be met under paragraph 8 continue to apply and must be satisfied for the replacement of main residence exception to apply.

LTTA/8130 Rules where former only or main residence sold within filing period for acquisition of new only or main residence

(paragraph 23 Schedule 5)

Where, at the end of the day of the effective date of the transaction, a taxpayer has interests in more than one dwelling they must self-assess the tax payable, subject to the replacement of a main residence rules, by using the higher rates of LTT. Special rules apply where the taxpayer owns a main residence and the new dwelling acquired is intended to be their new main residence.

In cases where the taxpayer would be entitled to amend their return or claim a repayment of the higher rates of LTT because they have sold their former main residence the taxpayer is entitled to self-assess the transaction acquiring the new main residence to main rates of LTT when the following conditions are met:

- the sale of the former main residence occurs within the filing period for the acquisition of the new main residence, and

- the return for that acquisition has not yet been made

The return for the acquisition of the new main residence must be made after the sale of the old main residence has occurred. The return cannot be made in anticipation of the subsequent sale (even where that is to occur on the same day as the return is filed, unless the sale transaction has competed).

LTTA/8140 Intermediate transactions

(paragraphs 9, 18 and 24 Schedule 5)

The LTT higher rates include rules that cover situations where the taxpayer sells a main residence, purchases a dwelling that is not intended to be a main residence on the effective date (or in any case before), they then subsequently purchase a main residence to which the taxpayer wishes to apply the main residence exclusions. The transaction effecting the acquisition of a dwelling acquired between the sale of the old main residence and the acquisition of the new main residence is called an ‘intermediate transaction’.

Without these rules, it may be possible for the taxpayer to structure their purchases in such a manner that they can purchase 2 dwellings, neither of which is subject to the higher rates. The LTT intermediate transaction rules have been designed to ensure that the tax payable on the intermediate transaction must be reappraised in certain circumstances.

An intermediate transaction is a higher rates residential property transaction if the intermediate transaction rules apply in relation to any one of the buyers.

The intermediate transaction rules apply where:

- the buyer in an intermediate transaction replaces their main residence in another transaction within 3 years of the disposal of their previous only or main residence, and

- that intermediate transaction occurs during the interim period

The interim period commences on the effective date of the transaction, effecting the disposal of the previous only or main residence, and ends on the effective date of a transaction to which the replacement of main residence exemption applies, or to which paragraph 3(6) of Schedule 4ZA to the Finance Act 2003 applies (SDLT), or paragraph 2(2) of Schedule 2A to the Land and Buildings Transaction Tax (Scotland) Act 2013 applies.

LTTA/8150 Interest acquired in the same main residence

(paragraphs 7 and 16 Schedule 5)

This exclusion for the LTT higher rates applies where the main subject matter of the transaction is a major interest in a dwelling where:

- immediately before the effective date of the transaction, the buyer or their spouse or civil partner already held a major interest in it, and

- immediately before and after the effective date of the transaction, that dwelling is the buyer’s only or main residence

The exclusion from the higher rates rules for these transactions ensures that the higher rates are not applied to a transaction where a major interest in the only or main residence is already held by the buyer (or their spouse or civil partner) and then another interest or a different interest is acquired in or over it.

For example, if a property is owned jointly by spouses and one co-owner transfers the whole of their interest to the other, who resides in the dwelling as their main residence, then the higher rates will not apply.

The also includes cases where the taxpayer surrenders and is re-granted a lease on their main residence (and owns other dwellings as well) as well as where the taxpayer acquires a lease extension which is granted as a new but separate reversionary lease.

The rules do not cover cases where a person acquires a different or additional interest in a dwelling that is not a main residence. Therefore if a person who owns a number of dwellings extends the lease on a dwelling that is not their main residence, they will, assuming the chargeable consideration is £40,000 or greater, be liable to the LTT higher rates on that land transaction.

LTTA/8160 Spouses and civil partners buying alone

(paragraph 25 Schedule 5)

Where a person is:

- married or in a civil partnership

- the couple are living together on the date of the acquisition, and

- only 1 of the spouses or civil partners is acquiring the major interest either solely or with other individuals

then both spouses and civil partners are deemed to be buyers. Their or their minor child’s interests in any dwellings need to be considered to establish if the transaction is a higher rates residential property transaction.

Taxpayers who are married or in a civil partnership are treated as living together unless they are separated:

- under an order of a court of competent jurisdiction (for example the family court in Wales or such similar court in another country)

- by a deed of separation, or

- in fact and the circumstances are such that the separation is likely to be permanent

LTTA/8170 Property adjustment on divorce, dissolution of civil partnership etc.

(paragraphs 26 Schedule 5)

The application of the LTT higher rates, for individuals, is dependent upon identifying the interests that the individual holds or is deemed to hold in other dwellings. These rules provide an exclusion for certain interests which are retained as a result of a buyer owning an interest (as a tenant in common) with their former spouse or civil partner due to an order under:

- section 24(1)(b) of the Matrimonial Causes Act 1973

- section 17(1)(a)(ii) of the Matrimonial and Family Proceedings Act 1984

- paragraph 7(1)(b) of Schedule 5 to the Civil Partnership Act 2004, or

- paragraph 9 of Schedule 7 to the Civil Partnership Act 2004

This means that where an individual retains an interest in a dwelling as a result of 1 of the above 4 provisions (and that dwelling is not the individual’s only or main residence), that interest is not considered when establishing if the individual owns interests in additional dwellings.

The exclusion does not apply where a couple has separated, unless the interest is retained due to 1 of the above 4 court orders and the court order must be in place prior to the purchase of the new dwelling.

A consent order which makes a property adjustment under 1 of the above 4 provisions is considered as being an order under 1 of the above 4 provisions.

If a court order is granted under 1 of the 4 provisions above after the individual has purchased a new property, it is not possible to claim a repayment for any higher rates tax paid on the purchase.

LTTA/8180 Settlements and Bare Trusts

(paragraphs 27, 28, 29, 30 and 31 Schedule 5)

LTTA/8190 Bare trusts and settlements – beneficiary deemed to be buyer or owner

(paragraphs 27 and 28 Schedule 5)

The treatment of purchases of additional residential dwellings, for the purposes of the higher rates provisions, differs depending on whether the trustee is the trustee of a bare trust, a trust entitling the beneficiary to occupy the dwelling for life or income earned in respect of the dwelling or any other trust (a ‘settlement’).

Where:

- a major interest in a dwelling, including the grant of a lease, or more than 1 dwelling is acquired

- by a trustee, or a number of trustees, of a settlement, alone or with others who are not trustees, and

- under the terms of the settlement the beneficiary (or beneficiaries) are entitled to occupy the dwelling for life or are entitled to the income earned;

then in order to establish the liability to the higher rates, it is necessary to look at the beneficiaries to establish, if they had acquired the dwelling rather than the trust, they would be liable to the LTT higher rates. If the beneficiaries (or any one of them) would have been liable to pay the LTT higher rates then the trustee(s) must file their return including a self assessment calculated using the LTT higher rates.

The beneficiary’s interest in dwellings also needs to be considered where there is a grant of a lease and the buyer is acting as a trustee of a bare trust. This is to ensure that leases cannot be granted to bare trustees and the usual rules relating to such a grant are not exploited to avoid the LTT higher rates applying.

Similarly, where:

- a person is the beneficiary under a settlement

- a major interest in a dwelling forms part of the trust property, and

- under the terms of the settlement the beneficiary (or beneficiaries) are entitled to occupy the dwelling for life or are entitled to the income earned

or where:

- a person is a beneficiary under a bare trust and a term of years absolute (that is a lease whether acquired by grant or assignment), in a dwelling forms part of the trust property;

then in order to establish the liability to the higher rates it is necessary to look at the beneficiaries to establish if they held the interest in the dwelling rather than the trust. Therefore, for the purposes of establishing the ownership, or disposal of, interests held a person will be treated as owning, or disposing of interests in dwellings held or disposed by the trust.

LTTA/8200 Tax liability of individuals who are trustees of settlement

(paragraph 31 Schedule 5)

Where:

- a major interest in a dwelling, or more than 1 dwelling is acquired

- by a trustee, or a number of trustees, of a settlement, alone or with others who are not trustees

- that trustee is an individual (or all the trustees are individuals), and

- under the terms of the settlement the beneficiary (or beneficiaries) are not entitled to occupy the dwelling for life or are not entitled to the income earned

then the trustee is treated as the beneficial owner and, despite them being an individual (or individuals) their acquisition, holding or disposal of a major interest in a dwelling is treated in the same manner as if that trustee was not an individual.

That is to say, if the conditions set out above are met, the acquisition of any major interest in a dwelling will be liable to LTT higher rates in so far as it meets the fundamental requirements for the higher rates to apply (consideration given is £40,000 or more) and none of the exclusions apply (for example the interest is subject to a lease with an unexpired term of greater than 21 years).

LTTA/8210 Acquisition by parent for minor child

(paragraph 30 Schedule 5)

Where a parent acquires a dwelling for a minor child then the parent, or any spouse or civil partner of the parent, (including step-parents), is to be treated as the buyer, or as holding or disposing of the interest rather than the child. The connection rule to the spouse or civil partner of the child is only relevant if the married couple or civil partners are living together.

However, it should be noted that in any case both natural parents will be considered to be the parent of the child so, whether living together or not, the natural parents are treated as acquiring, owning or disposing of the interest in the minor child’s dwelling even where the dwelling is being funded by just one of the parents.

LTTA/8220 Acquisition by Court appointed deputy for minor child

(paragraph 30 Schedule 5)

A special rule is provided so that the normal rule that a parent of the child is deemed to buy, hold or dispose of a dwelling does not apply where the buyer or owner is a deputy appointed by a court under section 16 of the Mental Capacity Act 2005, or a person appointed under a similar provision in a country outside Wales and England. The dwelling must have been acquired in the child’s name or on behalf of the child.

To qualify for the exclusion from the LTT higher rates the interest does not need to be acquired, held or disposed of solely by a court appointed deputy (or deputies), but one of the persons acquiring the dwelling must be a court appointed deputy. Such other owners could, for example, include the child’s parents or other relatives or guardians.

Where a dwelling is acquired, held or disposed of by a deputy, that dwelling is not treated for the purposes of the LTT higher rates as if it were the child’s parents’ interest. Rather, exceptionally, the interest is treated as though, for the purposes of establishing the rates applicable to the transaction, or the interests in dwellings owned by the child’s parents, as though it is acquired or owned by the child.

It is therefore possible for the parents of a child who has a court appointed deputy, to own an interest in a dwelling and for the child to acquire an interest in a dwelling through their deputy and for the child’s purchase not to be liable to the LTT higher rates. However, a second acquisition by the deputy on behalf of the child would potentially be liable to the LTT higher rates.

Essentially, the child who has a court appointed deputy is treated, for the purposes of the LTT higher rates as though they are an adult. Their land transactions and their ownership of dwellings for the purposes of the LTT higher rates, are disconnected from their parent’s acquisitions and ownership of interests in dwellings.

LTTA/8230 Major interests in dwellings inherited

(paragraph 34 Schedule 5)

Where a taxpayer inherits an interest in a dwelling and that interest represents greater than 50% of the value of the interest, then the interest will be treated as owned by the taxpayer from the date of the inheritance. A taxpayer will be treated as owning a beneficial share of more than 50% if:

- they are, individually, entitled to an interest that is greater than 50%

- the taxpayer and their spouse or civil partner taken together own, as tenants in common, an interest of greater than 50%, or

- the dwelling is owned by no more than 3 joint tenants and 2 of those joint tenants are the taxpayer and their spouse or civil partner.

It should be noted that any interests owned by minor children will be deemed as owned by their parent unless that interest is held as a result of an acquisition made by a court appointed deputy.

Where the inherited interest is of 50% or less (owned by the taxpayer or, where relevant, taken together with interests owned by the taxpayer’s spouse or civil partner), it will not immediately be treated as an interest in another dwelling for the purposes of the higher rates rules. Instead, it will be treated as an interest owned in another dwelling only from 3 years after the date of inheritance. However, if during that 3 year period the taxpayer’s interest in the dwelling changes through:

- a variation of a disposition

- acquiring other interests in the dwelling, or

- marriage or entering into a civil partnership

then if the interest is greater than 50% it will, immediately be treated as a major interest for the purposes of the higher rates legislation.

The date of the inheritance means the date on which the individual acquires the interest and that acquisition is in or towards satisfaction of an entitlement under or in relation to the will, or the intestacy, of a deceased person.

Special rules in relation to the date of inheritance, apply where there has been a variation of a disposition. Where such a variation occurs within 2 years of the person’s death then the date of inheritance is taken to be the date of acquisition in accordance with the variation.

LTTA/8240 Alternative finance arrangements

(paragraph 33 Schedule 5)

Where the dwelling is the subject of an alternative property finance arrangement, in relation to the ‘first transaction’ the person rather than the financial institution, is to be treated as the buyer for the purposes of establishing if the transaction is liable to the LTT higher rates. In the absence of this rule, every transaction entered into by the financial institution in relation to alternative property finance arrangements, would be liable to the higher rates as it would be the financial institution which would be considered to establish if it was liable to the higher rates, and not the person who has entered the arrangement with the financial institution.

LTTA/8250 Partnerships – interests acquired by a partner

(paragraph 32 Schedule 5)

Note: ‘Partner‘ and ‘partnership’ in this section refer to business partners and not to spouses, civil partners or those co-habiting (where the spouse or civil partner is also a business partner then that will be made clear in the examples).

Where a partner (who is an individual) in a partnership acquires a major interest in a dwelling either solely or jointly with other individuals and the dwelling is not being acquired for the purposes of the partnership, special rules apply. An example of this would be where the partner acquires their only or main residence, or where they acquire a buy-to-let property.

That rule is that any major interests held by or on behalf of the partnership for the purposes of the trade are not treated as held by or on behalf of the partner. Therefore, if a partnership that trades as a property developer or a business that owns major interests in dwellings for the purpose of their trade, (for example a farming business) those interests are not treated as held by the individual partners.

However, where a property is owned through a partnership and that property is used in a property letting business, the major interests in that dwelling are not used in a trade and the partner’s interest in that property will be treated as a major interest owned by the partner.

It should also be remembered that the property acquired by a partnership is treated as acquired by the partners (see LTTA 5080). Therefore, when a partnership acquires a dwelling (for any purpose), it will be important to establish whether that purchase is liable to pay the LTT higher rates. In order to establish this, it will be important know whether any of the partners own major interests in dwellings for the purposes of establishing liability to LTT higher rates for the partnership acquisition.

LTTA/8260 Major interest is subject to a lease

(paragraphs 3, 13 and 21 Schedule 5)

If the major interest acquired is subject to a lease, this can have an impact as to whether the transaction will be liable to the higher rates of LTT. A transaction will not be treated as a higher rates residential property transaction if, at the end of the effective date of the transaction the following conditions are met:

- the interest purchased was subject to a lease

- the main subject matter of the transaction is reversionary on that lease

- the lease has an unexpired term of more than 21 years, and

- the lease is not held by a person connected with the buyer

A person is connected to the buyer if they meet the conditions set out in Section 1122 of the Corporation Tax Act 2010.

The effect of the property being subject to a lease at the end of the day of the effective date of the transaction, is the same for an individual (or individuals) buying a single dwelling, or a number of dwellings in a single transaction, or where the buyer, or 1 of the buyers, is not an individual.

Recorded webinars

Watch our short explainer videos on higher rates.